MONTHLY QUOTE

“The optimist sees the rose and not its thorns; the pessimist stares at the thorns, oblivious of the rose.”

– Kahlil Gibran

MONTHLY TIP

Almost all business insurance policies require you to notify the insurer of an accident within 24 or 48 hours. Sometimes you can file the claim later, but you must report the incident within the stated window of time or risk forfeiting the right of recovery.

MONTHLY RIDDLE

Suzy and Ben stand upon a 200-foot cliff. They both slip down the cliff to the rocks below, but they have dinner together the next day. How can this be?

Last month’s riddle

It will let you enter, but not come in. It lets you create space, but it will never offer you a room. It has keys, but they open no locks. What is it?

Last month’s answer:

A computer.

THE MONTH IN BRIEF

Financially speaking, the last month of 2017 was also the year’s most newsworthy. Congress reformed federal tax law to a degree unseen since the 1980s, the Federal Reserve raised the benchmark interest rate, and bitcoin took its investors for a wild ride. Hiring, retail sales, and personal spending numbers were all impressive, as were consumer confidence index readings. The residential real estate market showed more momentum. Oil closed above $60 again. Emerging stock markets rallied; European equity benchmarks struggled. As all this transpired, the S&P 500 gained nearly 1%.(1)

DOMESTIC ECONOMIC HEALTH

On December 22, President Trump signed the Tax Cuts & Jobs Act into law. The new legislation amounted to a dramatic rewrite of key federal tax code provisions: it doubled the individual estate tax exemption to $11.2 million, raised the standard income tax deduction to $12,000, and eliminated the personal exemption as well as scores of deductions favored by taxpayers who itemize. The law also cut the corporate tax rate to 21% and permitted most pass-through businesses to take a 20% deduction on earnings. Most of these changes are scheduled to expire after 2025, unless Congress preserves them.(2)

The Federal Open Market Committee voted 7-2 to lift the benchmark interest rate another quarter of a point. That put the target range for the federal funds rate at 1.25-1.5%. The FOMC maintained its forecast for three rate hikes in 2018, with a consensus projection of the federal funds rate at 2.1% at the end of this year.(3)

As the fourth quarter ended, the third estimate of Q3 growth came in from the Bureau of Economic Analysis: a strong 3.2%, down from the prior 3.3%. In a good sign for Q4 GDP, personal spending rose 0.6% in November, with personal incomes up 0.3%. Looking ahead, the Federal Reserve’s median forecast sees the economy growing 2.5% in 2018.(3,4)

Speaking of growth, the factory and service sectors of the economy continued to expand nicely. The Institute for Supply Management’s manufacturing purchasing manager index came in at 58.2 for November; ISM’s non-manufacturing PMI showed a November reading of 57.4. (In October, the readings had been even higher. The factory PMI was up at 58.7; the services PMI, at 60.1.) Complementing this data, the federal government noted a 1.3% gain in hard goods orders in November.(4,5)

The country’s most-watched consumer confidence gauges were in good shape, though both declined in December. Economists polled by MarketWatch expected a reading of 127.5 for the Conference Board’s barometer and 97.1 for the University of Michigan’s index of consumer sentiment. The CB index fell 6.5 points to 122.1; the UMich index, 0.9 points from its preliminary December reading to 95.9.(3,4)

Confident consumers tend to spend freely, and that was the case during the holidays. The Department of Commerce found retail sales up 0.8% for November, and Adobe Digital Insights reported a 14.7% year-over-year rise in e-commerce sales in December.(6)

How about hiring? The latest Department of Labor employment snapshot showed a net gain of 228,000 jobs during November, with yearly wage growth of 2.5%. With hurricanes and floods no longer impeding payroll gains, October-November 2017 was the best two-month hiring period since mid-2016 (companies added a net 244,000 workers in the year’s tenth month). Headline unemployment remained at 4.1%, and the U-6 rate (unemployed + underemployed) was 0.1% higher at 8.0%.(3,7)

Headline and core inflation diverged in November: the main Consumer Price Index climbed 0.4%, yet the core CPI (minus energy and food prices) gained but 0.1%. For the year ending in November, the core CPI advanced only 1.7%; the headline CPI, 2.2%.(8)

GLOBAL ECONOMIC HEALTH

As 2017 ended, the European Union’s economy appeared to be stronger than it had been in some time. Its annual GDP was running at 2.5% through the third quarter, its jobless rate had fallen to 7.4% as of October, and annual inflation was at 1.8% in November. Recent developments affirm that the sovereign debt crisis is in the rear-view mirror. Burdened Greece finally had its credit rating upgraded by Fitch and Moody’s. Standard & Poor’s lifted Portugal’s credit rating from “junk” back to investment grade for the first time since 2012 and raised Italy’s credit rating for the first time since the 1980s. Even with the Brexit hanging over the eurozone’s collective head, journalists and other observers took to calling 2017 the year of the “euroboom.”(9,10)

While November reports on China’s factory production, business investment, and housing fell short of analyst expectations, its official manufacturing PMI did match the decent 51.6 forecast of economists surveyed by Reuters. China’s official Q3 GDP reading was released: 6.9%, topping government projections. In India, a rough economic year ended: a lingering cash shortage and a stumbling application of tax reforms helped drive the nation’s annualized GDP down below 6% at one juncture. (Economic growth had nearly reached 8% in 2016.) The International Monetary Fund has downgraded India’s 2018 growth forecast to 7.4% from 7.7%.(11,12)

WORLD MARKETS

Good news exceeded bad news in December. The MSCI Emerging Markets index climbed 3.36%, leaving its 2017 return at a striking 34.35%. The MSCI World advanced nicely as well – its 1.26% gain capped off a 20.11% annual rise. The Americas and the Asia-Pacific region saw many positive moves: a 3.05% gain for Brazil’s Bovespa, a 3.64% rise for Mexico’s Bolsa, and an 11.38% jump for Argentina’s MERVAL. India’s Nifty 50 added 1.63%; Canada’s TSX Composite, 1.51%; India’s Sensex, 1.35%. Australia’s All-Ordinaries gained 1.17%, while Hong Kong’s Hang Seng benchmark rose 1.00%. In Japan, the Nikkei 225 improved 0.74%. In Europe, Contrary to all this, the United Kingdom’s FTSE 100 soared 3.98%.(13,14)

The month’s notable declines were mainly in Europe – dips of 1.10% for the German DAX, 1.58% for the CAC 40 in France, and 2.18% for Spain’s IBEX 35. China’s Shanghai Composite lost 0.90%; Taiwan’s TSE 50, 1.58%, South Korea’s Kospi, 1.86%.(14)

MSCI’s Emerging Markets benchmark was not the only standout of 2017. The Hang Seng and the MERVAL, respectively, returned 37.30% and 81.57% year-over-year.(13,14)

COMMODITIES MARKETS

Bitcoin left cybercurrency investors queasy in December. The Commodity Futures Trading Commission approved bitcoin futures trading on the CBOE Global Markets and CME exchanges on December 1, and this new legitimacy helped the price almost double to nearly $20,000 by December 18. Then bitcoin dropped precipitously, partially recovering to $14,610 by the end of 2017’s final trading day. Turning to a different and far more stable kind of currency, the U.S. Dollar Index weakened 0.81% during December to 92.30.(15,16)

WTI crude ended 2017 at $60.10 a barrel, up 4.67% for December. Heating oil futures advanced 8.77% last month, and unleaded gasoline gained 3.42%; natural gas, on the other hand, slipped 2.25%. Cotton ruled ag futures with an 8.23% December improvement. Wheat gained 4.40%; corn, 2.71%. Other crops took minor or major falls: coffee lost 0.24%; sugar, 0.53%; soybeans, 3.37%; cocoa, 7.90%.(17)

What was gold worth at the end of 2017? An ounce was valued at $1,305.10 on the COMEX, thanks to a 2.42% December advance. Silver rose 3.79% on the month to wrap up 2017 at $16.98. Copper posted a 7.72% December gain; platinum, a 1.26% December loss.(17)

REAL ESTATE

Prices were high; inventory was thinner than it had been – and still, buyers found the homes they wanted. The annualized pace of existing home purchases rose 5.6% in November, and the rate of new home purchases accelerated 17.5%. The National Association of Realtors stated that resales were up 3.8% year-to-date; the median sale price was at $248,000, up 5.9% for the year. New home buying was up 22.8% year-over-year, according to the Census Bureau, with the annual increase at 31.1% in the west.(18)

If you found a home to buy, you probably found a cheap mortgage, historically speaking. Freddie Mac’s final Primary Mortgage Market Survey of 2018 did show rates climbing, however. In the December 28 PMMS, the average interest rate on a conventional home loan was 3.99%, up from 3.90% on November 30. In the same time frame, the average interest rate on the 15-year fixed went from 3.30% to 3.44%, and the mean interest on the 5/1-year ARM jumped from 3.32% to 3.47%.(19)

Now to the latest statistics on home construction. The Census Bureau reported a 3.3% gain for groundbreaking in November, with building permits down 1.4% (but there was a 1.4% rise for single-family permits).(18)

LOOKING BACK…LOOKING FORWARD

Blue chips led the way in December: the Dow Jones Industrial Average added 1.84% last month, far outpacing the S&P 500 (+0.98%), the Nasdaq Composite (+0.43%), and the Russell 2000 (-0.53%).(1,20)

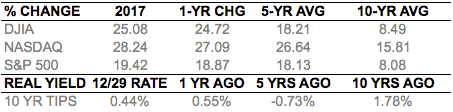

As the table below notes, the Dow also recorded the best 2017 gain of the big three. (The Russell 2000 rose 13.14% on the year.) At the closing bell on December 29, the settlements were: Dow, 24,719.22; S&P, 2,673.61; Nasdaq, 6,903.39; Russell, 1,535.51.(20,21)

The CBOE VIX, which gauges volatility in the markets, had a poor year: it fell 21.37% to 11.04. The NYSE Arca Biotech index had a phenomenal 2017, climbing 37.31%.(21)

Indices are unmanaged, do not incur fees or expenses, and cannot be invested into directly. These returns do not include dividends. 10-year TIPS real yield = projected return at maturity given expected inflation.

In hindsight, we look back at 2017 and see a year that surpassed expectations. You could say the stars aligned for Wall Street: no news events truly disrupted the markets, inflation remained tame, the dollar weakened, and the economic recovery gained further momentum. Will 2018 be as great as 2017 was? Probably not, in the view of analysts. Many are predicting just a single-digit advance for the S&P 500 (Kiplinger’s Personal Finance, to cite but one forecast, projects a 2018 total return of just 8% for the benchmark). While fundamental economic indicators are strong, Fed policymakers could tighten faster if wage growth and inflation accelerate. The Fed is continuing to thin its balance sheet, and the European Central Bank seems poised to end its long-running stimulus. The last S&P 500 correction, a 14% drop, occurred in early 2016; the index is long overdue for another. If the bull market lasts into September, it will be the longest ever witnessed. Some strong headwinds could arise in 2018; prepare for some turbulence, which will arrive at some point, and be glad for the sizable stock gains of 2017.(25)

UPCOMING ECONOMIC RELEASES: Across the rest of January, investors will pay attention to these news items: December’s ADP payrolls report and Challenger job-cut report (1/4), the latest employment snapshot from the Department of Labor and a new ISM service sector PMI (1/5), the latest wholesale inflation reading (1/11), the initial January University of Michigan consumer sentiment index, the December CPI and December retail sales (1/12), December industrial production (1/17), December housing starts and building permits (1/18), December existing home sales (1/24), December new home sales and the Conference Board’s latest leading indicator index (1/25), December hard goods orders, the month’s final University of Michigan consumer sentiment index reading, and the first estimate of Q4 economic growth (1/26), the December PCE price index and December personal spending (1/29), the Conference Board’s January consumer confidence index (1/30), and lastly, a policy statement from the Federal Reserve, the January ADP payrolls report, and the NAR’s December pending home sales index (1/31).

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. The information herein has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. Investments will fluctuate and when redeemed may be worth more or less than when originally invested. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All market indices discussed are unmanaged and are not illustrative of any particular investment. Indices do not incur management fees, costs and expenses, and cannot be invested into directly. All economic and performance data is historical and not indicative of future results. The Dow Jones Industrial Average is a price-weighted index of 30 actively traded blue-chip stocks. The NASDAQ Composite Index is a market-weighted index of all over-the-counter common stocks traded on the National Association of Securities Dealers Automated Quotation System. The Standard & Poor’s 500 (S&P 500) is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy. The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. The CBOE Volatility Index® (VIX®) is a key measure of market expectations of near-term volatility conveyed by S&P 500 stock index option prices. NYSE Group, Inc. (NYSE:NYX) operates two securities exchanges: the New York Stock Exchange (the “NYSE”) and NYSE Arca (formerly known as the Archipelago Exchange, or ArcaEx®, and the Pacific Exchange). NYSE Group is a leading provider of securities listing, trading and market data products and services. The New York Mercantile Exchange, Inc. (NYMEX) is the world’s largest physical commodity futures exchange and the preeminent trading forum for energy and precious metals, with trading conducted through two divisions – the NYMEX Division, home to the energy, platinum, and palladium markets, and the COMEX Division, on which all other metals trade. The MSCI Emerging Markets Index is a float-adjusted market capitalization index consisting of indices in more than 25 emerging economies. The MSCI World Index is a free-float weighted equity index that includes developed world markets, and does not include emerging markets. The Bovespa Index is a gross total return index weighted by traded volume & is comprised of the most liquid stocks traded on the Sao Paulo Stock Exchange. The Mexican Stock Exchange, commonly known as Mexican Bolsa, Mexbol, or BMV, is the only stock exchange in Mexico. The MERVAL Index (MERcado de VALores, literally Stock Exchange) is the most important index of the Buenos Aires Stock Exchange. The Nifty 50 (NTFE 50) is a well-diversified 50-stock index accounting for 13 sectors of the Indian economy. It is used for a variety of purposes such as benchmarking fund portfolios, index-based derivatives and index funds. The S&P/TSX Composite Index is an index of the stock (equity) prices of the largest companies on the Toronto Stock Exchange (TSX) as measured by market capitalization. The BSE SENSEX (Bombay Stock Exchange Sensitive Index), also-called the BSE 30 (BOMBAY STOCK EXCHANGE) or simply the SENSEX, is a free-float market capitalization-weighted stock market index of 30 well-established and financially sound companies listed on the Bombay Stock Exchange (BSE). The All Ordinaries (XAO) is considered a total market barometer for the Australian stock market and contains the 500 largest ASX-listed companies by way of market capitalization. The Hang Seng Index is a free float-adjusted market capitalization-weighted stock market index that is the main indicator of the overall market performance in Hong Kong. Nikkei 225 (Ticker: ^N225) is a stock market index for the Tokyo Stock Exchange (TSE). The Nikkei average is the most watched index of Asian stocks. The FTSE 100 Index is a share index of the 100 companies listed on the London Stock Exchange with the highest market capitalization. The DAX 30 is a Blue-Chip stock market index consisting of the 30 major German companies trading on the Frankfurt Stock Exchange. The CAC-40 Index is a narrow-based, modified capitalization-weighted index of 40 companies listed on the Paris Bourse. The IBEX 35 is the benchmark stock market index of the Bolsa de Madrid, Spain’s principal stock exchange. The SSE Composite Index is an index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange. The FTSE TWSE Taiwan 50 Index consists of the largest 50 companies by full market value, and is also the first narrow-based index published in Taiwan. The Korea Composite Stock Price Index or KOSPI is the major stock market index of South Korea, representing all common stocks traded on the Korea Exchange. The US Dollar Index measures the performance of the U.S. dollar against a basket of six currencies. The NYSE Arca Biotechnology IndexSM is an equal dollar weighted index designed to measure the performance of a cross section of companies in the biotechnology industry that are primarily involved in the use of biological processes to develop products or provide services Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. MarketingPro, Inc. is not affiliated with any person or firm that may be providing this information to you. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional.

Citations.

1 – us.spindices.com/indices/equity/sp-500 [12/29/17]

2 – cpapracticeadvisor.com/news/12388205/2018-tax-reform-law-new-tax-brackets-credits-and-deductions [12/22/17]

3 – bloomberg.com/news/articles/2017-12-13/fed-raises-rates-while-sticking-to-three-hike-outlook-for-2018 [12/13/17]

4 – marketwatch.com/economy-politics/calendars/economic [12/29/17]

5 – instituteforsupplymanagement.org/ISMReport/NonMfgROB.cfm?SSO=1 [12/5/17]

6 – latimes.com/business/la-fi-retail-apocalypse-20171225-story.html [12/25/17]

7 – fortune.com/2017/12/08/november-job-report-unemployment-rate/ [12/8/17]

8 – reuters.com/article/us-usa-economy-inflation/u-s-core-inflation-slows-puts-spotlight-on-2018-interest-rate-outlook-idUSKBN1E71QM [12/13/17]

9 – ec.europa.eu/eurostat [12/29/17]

10 – qz.com/1163174/the-economic-surprise-of-2017-was-europes-best-year-in-a-decade/ [12/25/17]

11 – asia.nikkei.com/Politics-Economy/Economy/China-s-December-factory-PMI-dips-to-51.6-hitting-forecasts [12/31/17]

12 – bbc.com/news/world-asia-india-42510563 [12/30/17]

13 – msci.com/end-of-day-data-search [12/29/17]

14 – markets.on.nytimes.com/research/markets/worldmarkets/worldmarkets.asp [12/29/17]

15 – tinyurl.com/y7f355aq [12/31/17]

16 – marketwatch.com/investing/index/dxy/historical [12/29/17]

17 – money.cnn.com/data/commodities/ [12/29/17]

18 – quickenloans.com/blog/mostly-cheery-economic-week-market-update [12/26/17]

19 – freddiemac.com/pmms/archive.html?year=2017 [12/29/17]

20 – finance.google.com/finance?q=INDEXDJX%3A.DJI&ei=sM5GWunuMYPE2Ab8xo-YDg [12/29/17]

21 – markets.wsj.com/us [12/29/17]

22 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=12%2F29%2F16&x=0&y=0 [12/29/17]

22 – bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=12%2F29%2F16&x=0&y=0 [12/29/17]

22 – bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=12%2F29%2F16&x=0&y=0 [12/29/17]

22 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=12%2F28%2F12&x=0&y=0 [12/29/17]

22 – bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=12%2F28%2F12&x=0&y=0 [12/29/17]

22 – bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=12%2F28%2F12&x=0&y=0 [12/29/17]

22 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=12%2F28%2F07&x=0&y=0 [12/29/17]

22 – bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=12%2F28%2F07&x=0&y=0 [12/29/17]

22 – bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=12%2F28%2F07&x=0&y=0 [12/29/17]

23 – treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyield [12/29/17]

24 – treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyieldAll [12/29/17]

25 – kiplinger.com/article/investing/T052-C008-S002-where-to-invest-in-2018.html [1/18]

Other Information:

Adams Wealth Management Group LLC (“Adams Wealth Management”) is a registered investment adviser offering advisory services in the State of Texas and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. The presence of this website on the Internet shall not be directly or indirectly interpreted as a solicitation of investment advisory services to persons of another jurisdiction unless otherwise permitted by statute. Follow-up or individualized responses to consumers in a particular state by Adams Wealth Management in the rendering of personalized investment advice for compensation shall not be made without our first complying with jurisdiction requirements or pursuant an applicable state exemption.

All written content on this site is for information purposes only. Opinions expressed herein are solely those of Adams Wealth Management, unless otherwise specifically cited. Material presented is believed to be from reliable sources and no representations are made by our firm as to another parties’ informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant or legal counsel prior to implementation.

All investing involves risk, including the potential for loss of principal. There is no guarantee that any investment strategy or plan will be successful.

THE MONTH IN BRIEF

Financially speaking, the last month of 2017 was also the year’s most newsworthy. Congress reformed federal tax law to a degree unseen since the 1980s, the Federal Reserve raised the benchmark interest rate, and bitcoin took its investors for a wild ride. Hiring, retail sales, and personal spending numbers were all impressive, as were consumer confidence index readings. The residential real estate market showed more momentum. Oil closed above $60 again. Emerging stock markets rallied; European equity benchmarks struggled. As all this transpired, the S&P 500 gained nearly 1%.(1)

DOMESTIC ECONOMIC HEALTH

On December 22, President Trump signed the Tax Cuts & Jobs Act into law. The new legislation amounted to a dramatic rewrite of key federal tax code provisions: it doubled the individual estate tax exemption to $11.2 million, raised the standard income tax deduction to $12,000, and eliminated the personal exemption as well as scores of deductions favored by taxpayers who itemize. The law also cut the corporate tax rate to 21% and permitted most pass-through businesses to take a 20% deduction on earnings. Most of these changes are scheduled to expire after 2025, unless Congress preserves them.(2)

The Federal Open Market Committee voted 7-2 to lift the benchmark interest rate another quarter of a point. That put the target range for the federal funds rate at 1.25-1.5%. The FOMC maintained its forecast for three rate hikes in 2018, with a consensus projection of the federal funds rate at 2.1% at the end of this year.(3)

As the fourth quarter ended, the third estimate of Q3 growth came in from the Bureau of Economic Analysis: a strong 3.2%, down from the prior 3.3%. In a good sign for Q4 GDP, personal spending rose 0.6% in November, with personal incomes up 0.3%. Looking ahead, the Federal Reserve’s median forecast sees the economy growing 2.5% in 2018.(3,4)

Speaking of growth, the factory and service sectors of the economy continued to expand nicely. The Institute for Supply Management’s manufacturing purchasing manager index came in at 58.2 for November; ISM’s non-manufacturing PMI showed a November reading of 57.4. (In October, the readings had been even higher. The factory PMI was up at 58.7; the services PMI, at 60.1.) Complementing this data, the federal government noted a 1.3% gain in hard goods orders in November.(4,5)

The country’s most-watched consumer confidence gauges were in good shape, though both declined in December. Economists polled by MarketWatch expected a reading of 127.5 for the Conference Board’s barometer and 97.1 for the University of Michigan’s index of consumer sentiment. The CB index fell 6.5 points to 122.1; the UMich index, 0.9 points from its preliminary December reading to 95.9.(3,4)

Confident consumers tend to spend freely, and that was the case during the holidays. The Department of Commerce found retail sales up 0.8% for November, and Adobe Digital Insights reported a 14.7% year-over-year rise in e-commerce sales in December.(6)

How about hiring? The latest Department of Labor employment snapshot showed a net gain of 228,000 jobs during November, with yearly wage growth of 2.5%. With hurricanes and floods no longer impeding payroll gains, October-November 2017 was the best two-month hiring period since mid-2016 (companies added a net 244,000 workers in the year’s tenth month). Headline unemployment remained at 4.1%, and the U-6 rate (unemployed + underemployed) was 0.1% higher at 8.0%.(3,7)

Headline and core inflation diverged in November: the main Consumer Price Index climbed 0.4%, yet the core CPI (minus energy and food prices) gained but 0.1%. For the year ending in November, the core CPI advanced only 1.7%; the headline CPI, 2.2%.(8)

GLOBAL ECONOMIC HEALTH

As 2017 ended, the European Union’s economy appeared to be stronger than it had been in some time. Its annual GDP was running at 2.5% through the third quarter, its jobless rate had fallen to 7.4% as of October, and annual inflation was at 1.8% in November. Recent developments affirm that the sovereign debt crisis is in the rear-view mirror. Burdened Greece finally had its credit rating upgraded by Fitch and Moody’s. Standard & Poor’s lifted Portugal’s credit rating from “junk” back to investment grade for the first time since 2012 and raised Italy’s credit rating for the first time since the 1980s. Even with the Brexit hanging over the eurozone’s collective head, journalists and other observers took to calling 2017 the year of the “euroboom.”(9,10)

While November reports on China’s factory production, business investment, and housing fell short of analyst expectations, its official manufacturing PMI did match the decent 51.6 forecast of economists surveyed by Reuters. China’s official Q3 GDP reading was released: 6.9%, topping government projections. In India, a rough economic year ended: a lingering cash shortage and a stumbling application of tax reforms helped drive the nation’s annualized GDP down below 6% at one juncture. (Economic growth had nearly reached 8% in 2016.) The International Monetary Fund has downgraded India’s 2018 growth forecast to 7.4% from 7.7%.(11,12)

WORLD MARKETS

Good news exceeded bad news in December. The MSCI Emerging Markets index climbed 3.36%, leaving its 2017 return at a striking 34.35%. The MSCI World advanced nicely as well – its 1.26% gain capped off a 20.11% annual rise. The Americas and the Asia-Pacific region saw many positive moves: a 3.05% gain for Brazil’s Bovespa, a 3.64% rise for Mexico’s Bolsa, and an 11.38% jump for Argentina’s MERVAL. India’s Nifty 50 added 1.63%; Canada’s TSX Composite, 1.51%; India’s Sensex, 1.35%. Australia’s All-Ordinaries gained 1.17%, while Hong Kong’s Hang Seng benchmark rose 1.00%. In Japan, the Nikkei 225 improved 0.74%. In Europe, Contrary to all this, the United Kingdom’s FTSE 100 soared 3.98%.(13,14)

The month’s notable declines were mainly in Europe – dips of 1.10% for the German DAX, 1.58% for the CAC 40 in France, and 2.18% for Spain’s IBEX 35. China’s Shanghai Composite lost 0.90%; Taiwan’s TSE 50, 1.58%, South Korea’s Kospi, 1.86%.(14)

MSCI’s Emerging Markets benchmark was not the only standout of 2017. The Hang Seng and the MERVAL, respectively, returned 37.30% and 81.57% year-over-year.(13,14)

COMMODITIES MARKETS

Bitcoin left cybercurrency investors queasy in December. The Commodity Futures Trading Commission approved bitcoin futures trading on the CBOE Global Markets and CME exchanges on December 1, and this new legitimacy helped the price almost double to nearly $20,000 by December 18. Then bitcoin dropped precipitously, partially recovering to $14,610 by the end of 2017’s final trading day. Turning to a different and far more stable kind of currency, the U.S. Dollar Index weakened 0.81% during December to 92.30.(15,16)

WTI crude ended 2017 at $60.10 a barrel, up 4.67% for December. Heating oil futures advanced 8.77% last month, and unleaded gasoline gained 3.42%; natural gas, on the other hand, slipped 2.25%. Cotton ruled ag futures with an 8.23% December improvement. Wheat gained 4.40%; corn, 2.71%. Other crops took minor or major falls: coffee lost 0.24%; sugar, 0.53%; soybeans, 3.37%; cocoa, 7.90%.(17)

What was gold worth at the end of 2017? An ounce was valued at $1,305.10 on the COMEX, thanks to a 2.42% December advance. Silver rose 3.79% on the month to wrap up 2017 at $16.98. Copper posted a 7.72% December gain; platinum, a 1.26% December loss.(17)

REAL ESTATE

Prices were high; inventory was thinner than it had been – and still, buyers found the homes they wanted. The annualized pace of existing home purchases rose 5.6% in November, and the rate of new home purchases accelerated 17.5%. The National Association of Realtors stated that resales were up 3.8% year-to-date; the median sale price was at $248,000, up 5.9% for the year. New home buying was up 22.8% year-over-year, according to the Census Bureau, with the annual increase at 31.1% in the west.(18)

If you found a home to buy, you probably found a cheap mortgage, historically speaking. Freddie Mac’s final Primary Mortgage Market Survey of 2018 did show rates climbing, however. In the December 28 PMMS, the average interest rate on a conventional home loan was 3.99%, up from 3.90% on November 30. In the same time frame, the average interest rate on the 15-year fixed went from 3.30% to 3.44%, and the mean interest on the 5/1-year ARM jumped from 3.32% to 3.47%.(19)

Now to the latest statistics on home construction. The Census Bureau reported a 3.3% gain for groundbreaking in November, with building permits down 1.4% (but there was a 1.4% rise for single-family permits).(18)

LOOKING BACK…LOOKING FORWARD

Blue chips led the way in December: the Dow Jones Industrial Average added 1.84% last month, far outpacing the S&P 500 (+0.98%), the Nasdaq Composite (+0.43%), and the Russell 2000 (-0.53%).(1,20)

As the table below notes, the Dow also recorded the best 2017 gain of the big three. (The Russell 2000 rose 13.14% on the year.) At the closing bell on December 29, the settlements were: Dow, 24,719.22; S&P, 2,673.61; Nasdaq, 6,903.39; Russell, 1,535.51.(20,21)

The CBOE VIX, which gauges volatility in the markets, had a poor year: it fell 21.37% to 11.04. The NYSE Arca Biotech index had a phenomenal 2017, climbing 37.31%.(21)

Indices are unmanaged, do not incur fees or expenses, and cannot be invested into directly. These returns do not include dividends. 10-year TIPS real yield = projected return at maturity given expected inflation.

In hindsight, we look back at 2017 and see a year that surpassed expectations. You could say the stars aligned for Wall Street: no news events truly disrupted the markets, inflation remained tame, the dollar weakened, and the economic recovery gained further momentum. Will 2018 be as great as 2017 was? Probably not, in the view of analysts. Many are predicting just a single-digit advance for the S&P 500 (Kiplinger’s Personal Finance, to cite but one forecast, projects a 2018 total return of just 8% for the benchmark). While fundamental economic indicators are strong, Fed policymakers could tighten faster if wage growth and inflation accelerate. The Fed is continuing to thin its balance sheet, and the European Central Bank seems poised to end its long-running stimulus. The last S&P 500 correction, a 14% drop, occurred in early 2016; the index is long overdue for another. If the bull market lasts into September, it will be the longest ever witnessed. Some strong headwinds could arise in 2018; prepare for some turbulence, which will arrive at some point, and be glad for the sizable stock gains of 2017.(25)

UPCOMING ECONOMIC RELEASES: Across the rest of January, investors will pay attention to these news items: December’s ADP payrolls report and Challenger job-cut report (1/4), the latest employment snapshot from the Department of Labor and a new ISM service sector PMI (1/5), the latest wholesale inflation reading (1/11), the initial January University of Michigan consumer sentiment index, the December CPI and December retail sales (1/12), December industrial production (1/17), December housing starts and building permits (1/18), December existing home sales (1/24), December new home sales and the Conference Board’s latest leading indicator index (1/25), December hard goods orders, the month’s final University of Michigan consumer sentiment index reading, and the first estimate of Q4 economic growth (1/26), the December PCE price index and December personal spending (1/29), the Conference Board’s January consumer confidence index (1/30), and lastly, a policy statement from the Federal Reserve, the January ADP payrolls report, and the NAR’s December pending home sales index (1/31).

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. The information herein has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. Investments will fluctuate and when redeemed may be worth more or less than when originally invested. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All market indices discussed are unmanaged and are not illustrative of any particular investment. Indices do not incur management fees, costs and expenses, and cannot be invested into directly. All economic and performance data is historical and not indicative of future results. The Dow Jones Industrial Average is a price-weighted index of 30 actively traded blue-chip stocks. The NASDAQ Composite Index is a market-weighted index of all over-the-counter common stocks traded on the National Association of Securities Dealers Automated Quotation System. The Standard & Poor’s 500 (S&P 500) is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy. The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. The CBOE Volatility Index® (VIX®) is a key measure of market expectations of near-term volatility conveyed by S&P 500 stock index option prices. NYSE Group, Inc. (NYSE:NYX) operates two securities exchanges: the New York Stock Exchange (the “NYSE”) and NYSE Arca (formerly known as the Archipelago Exchange, or ArcaEx®, and the Pacific Exchange). NYSE Group is a leading provider of securities listing, trading and market data products and services. The New York Mercantile Exchange, Inc. (NYMEX) is the world’s largest physical commodity futures exchange and the preeminent trading forum for energy and precious metals, with trading conducted through two divisions – the NYMEX Division, home to the energy, platinum, and palladium markets, and the COMEX Division, on which all other metals trade. The MSCI Emerging Markets Index is a float-adjusted market capitalization index consisting of indices in more than 25 emerging economies. The MSCI World Index is a free-float weighted equity index that includes developed world markets, and does not include emerging markets. The Bovespa Index is a gross total return index weighted by traded volume & is comprised of the most liquid stocks traded on the Sao Paulo Stock Exchange. The Mexican Stock Exchange, commonly known as Mexican Bolsa, Mexbol, or BMV, is the only stock exchange in Mexico. The MERVAL Index (MERcado de VALores, literally Stock Exchange) is the most important index of the Buenos Aires Stock Exchange. The Nifty 50 (NTFE 50) is a well-diversified 50-stock index accounting for 13 sectors of the Indian economy. It is used for a variety of purposes such as benchmarking fund portfolios, index-based derivatives and index funds. The S&P/TSX Composite Index is an index of the stock (equity) prices of the largest companies on the Toronto Stock Exchange (TSX) as measured by market capitalization. The BSE SENSEX (Bombay Stock Exchange Sensitive Index), also-called the BSE 30 (BOMBAY STOCK EXCHANGE) or simply the SENSEX, is a free-float market capitalization-weighted stock market index of 30 well-established and financially sound companies listed on the Bombay Stock Exchange (BSE). The All Ordinaries (XAO) is considered a total market barometer for the Australian stock market and contains the 500 largest ASX-listed companies by way of market capitalization. The Hang Seng Index is a free float-adjusted market capitalization-weighted stock market index that is the main indicator of the overall market performance in Hong Kong. Nikkei 225 (Ticker: ^N225) is a stock market index for the Tokyo Stock Exchange (TSE). The Nikkei average is the most watched index of Asian stocks. The FTSE 100 Index is a share index of the 100 companies listed on the London Stock Exchange with the highest market capitalization. The DAX 30 is a Blue-Chip stock market index consisting of the 30 major German companies trading on the Frankfurt Stock Exchange. The CAC-40 Index is a narrow-based, modified capitalization-weighted index of 40 companies listed on the Paris Bourse. The IBEX 35 is the benchmark stock market index of the Bolsa de Madrid, Spain’s principal stock exchange. The SSE Composite Index is an index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange. The FTSE TWSE Taiwan 50 Index consists of the largest 50 companies by full market value, and is also the first narrow-based index published in Taiwan. The Korea Composite Stock Price Index or KOSPI is the major stock market index of South Korea, representing all common stocks traded on the Korea Exchange. The US Dollar Index measures the performance of the U.S. dollar against a basket of six currencies. The NYSE Arca Biotechnology IndexSM is an equal dollar weighted index designed to measure the performance of a cross section of companies in the biotechnology industry that are primarily involved in the use of biological processes to develop products or provide services Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. MarketingPro, Inc. is not affiliated with any person or firm that may be providing this information to you. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional.

Citations.

1 – us.spindices.com/indices/equity/sp-500 [12/29/17]

2 – cpapracticeadvisor.com/news/12388205/2018-tax-reform-law-new-tax-brackets-credits-and-deductions [12/22/17]

3 – bloomberg.com/news/articles/2017-12-13/fed-raises-rates-while-sticking-to-three-hike-outlook-for-2018 [12/13/17]

4 – marketwatch.com/economy-politics/calendars/economic [12/29/17]

5 – instituteforsupplymanagement.org/ISMReport/NonMfgROB.cfm?SSO=1 [12/5/17]

6 – latimes.com/business/la-fi-retail-apocalypse-20171225-story.html [12/25/17]

7 – fortune.com/2017/12/08/november-job-report-unemployment-rate/ [12/8/17]

8 – reuters.com/article/us-usa-economy-inflation/u-s-core-inflation-slows-puts-spotlight-on-2018-interest-rate-outlook-idUSKBN1E71QM [12/13/17]

9 – ec.europa.eu/eurostat [12/29/17]

10 – qz.com/1163174/the-economic-surprise-of-2017-was-europes-best-year-in-a-decade/ [12/25/17]

11 – asia.nikkei.com/Politics-Economy/Economy/China-s-December-factory-PMI-dips-to-51.6-hitting-forecasts [12/31/17]

12 – bbc.com/news/world-asia-india-42510563 [12/30/17]

13 – msci.com/end-of-day-data-search [12/29/17]

14 – markets.on.nytimes.com/research/markets/worldmarkets/worldmarkets.asp [12/29/17]

15 – tinyurl.com/y7f355aq [12/31/17]

16 – marketwatch.com/investing/index/dxy/historical [12/29/17]

17 – money.cnn.com/data/commodities/ [12/29/17]

18 – quickenloans.com/blog/mostly-cheery-economic-week-market-update [12/26/17]

19 – freddiemac.com/pmms/archive.html?year=2017 [12/29/17]

20 – finance.google.com/finance?q=INDEXDJX%3A.DJI&ei=sM5GWunuMYPE2Ab8xo-YDg [12/29/17]

21 – markets.wsj.com/us [12/29/17]

22 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=12%2F29%2F16&x=0&y=0 [12/29/17]

22 – bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=12%2F29%2F16&x=0&y=0 [12/29/17]

22 – bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=12%2F29%2F16&x=0&y=0 [12/29/17]

22 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=12%2F28%2F12&x=0&y=0 [12/29/17]

22 – bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=12%2F28%2F12&x=0&y=0 [12/29/17]

22 – bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=12%2F28%2F12&x=0&y=0 [12/29/17]

22 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=12%2F28%2F07&x=0&y=0 [12/29/17]

22 – bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=12%2F28%2F07&x=0&y=0 [12/29/17]

22 – bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=12%2F28%2F07&x=0&y=0 [12/29/17]

23 – treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyield [12/29/17]

24 – treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyieldAll [12/29/17]

25 – kiplinger.com/article/investing/T052-C008-S002-where-to-invest-in-2018.html [1/18]

Other Information:

Adams Wealth Management Group LLC (“Adams Wealth Management”) is a registered investment adviser offering advisory services in the State of Texas and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. The presence of this website on the Internet shall not be directly or indirectly interpreted as a solicitation of investment advisory services to persons of another jurisdiction unless otherwise permitted by statute. Follow-up or individualized responses to consumers in a particular state by Adams Wealth Management in the rendering of personalized investment advice for compensation shall not be made without our first complying with jurisdiction requirements or pursuant an applicable state exemption.

All written content on this site is for information purposes only. Opinions expressed herein are solely those of Adams Wealth Management, unless otherwise specifically cited. Material presented is believed to be from reliable sources and no representations are made by our firm as to another parties’ informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant or legal counsel prior to implementation.

All investing involves risk, including the potential for loss of principal. There is no guarantee that any investment strategy or plan will be successful.