MONTHLY QUOTE

“If you don’t like something, change it. If you can’t change it, change your attitude.”

– Maya Angelou

MONTHLY TIP

Do you have a child or grandchild with a direct federal college loan? That loan may qualify for the Department of Education’s Public Service Loan Forgiveness Program, which forgives loans for borrowers who have worked in public service for 10 years and kept up payments during that decade.

MONTHLY RIDDLE

Suzanne, a hair stylist, says that given the choice, she would prefer to cut and style the hair of two redheads instead of one brunette. She says there is a logical reason why. What is it?

Last month’s riddle

Through families it runs, and through bodies it flows. What is it?

Last month’s answer:

Blood.

THE MONTH IN BRIEF

April saw the S&P 500 advance 0.27% as a new earnings season unfolded – one in which investors grew uneasy about rising Treasury yields, protectionism, and privacy concerns involving tech giants. While the financial media largely focused on those anxieties, good news also appeared. The latest consumer spending and consumer confidence data was solid. Home buying picked up as listings increased slightly. Oil rallied, and so did the dollar. Overseas equity benchmarks saw big gains, even as some economists wondered if the boom in global growth was fading. One of the major financial news stories of April broke only hours before the start of May: a postponement of the tariffs planned for imported metals.(1)

DOMESTIC ECONOMIC HEALTH

On the night of April 30, the Trump administration elected to delay the imposition of excise taxes on aluminum and steel imported to America from China, Mexico, Canada, Brazil, Argentina, Australia, and the European Union. Those tariffs were set to take effect on May 1, but they are now on hold until at least June 1 (2)

Consumer spending was strong in March, according to the Department of Commerce. Households devoted 0.4% more of their incomes to consumer purchases than they did in February (and household incomes rose 0.3%). Retail sales picked up 0.6% in March, quite a change from the 0.1% decline in February. The Bureau of Economic Analysis released its first estimate of first quarter GDP in late April: 2.3%.(3)

Consumer confidence indices ended the month on an upswing. The University of Michigan’s index had a final April reading of 98.8, a point higher than its initial April mark. The Conference Board’s index came in at 128.7, a rise of 1.7 points from March; it surpassed MarketWatch’s consensus forecast by 2.8 points.(3)

Inflation pressure was mounting: the year-over-year change in the Consumer Price Index was 2.4% through March, even with a 0.1% retreat for the headline CPI. (That compares to 2.2% annualized inflation in February.) The core CPI was up 2.1% in the 12 months ending in March, compared to a yearly gain of 1.8% a month previously. Annual wholesale inflation reached 3.0% as the first quarter ended. The March employment report from the Department of Labor showed wages keeping pace with consumer costs; they were rising at 2.7% annually.(4,5)

The rest of the March jobs report was disappointing. Employers added only 103,000 net new hires, the lowest monthly total in half a year. Some economists thought weather held hiring back in certain industries. The Department of Labor recorded unemployment at 4.1% for a sixth consecutive month; the good news was the 0.2% dip in the U-6 jobless rate that encompasses underemployed Americans. In March, the U-6 rate fell to 8.0%.(5)

Once again, expansion in the manufacturing and service industries impressed. The Institute for Supply Management’s twin purchasing manager indices were in the high fifties in March; they both declined from lofty February readings. ISM’s factory PMI descended to 59.3 in March from 60.8 and wound up at 57.3 in April. Its service sector PMI fell from 59.5 to 58.8 in March. Durable goods orders rose 2.6% for March.(3,6)

GLOBAL ECONOMIC HEALTH

Were seemingly healthy economies in Europe losing momentum? Investors, economists, and journalists noticed some deterioration in fundamentals. An index of German business confidence touched a low unseen in a year in April, echoing a drop in a broader eurozone index. Markit’s eurozone manufacturing PMI was 56.0 at last reading, but about five points lower than its late 2017 peak. The Baltic Dry Freight Index, a barometer of shipping activity, fell to an 8-month low in April. The yield curve for government bonds has been flattening in western economies, a signal of more pessimism than optimism. Still, some analysts call these declines seasonal, reflective of rough weather in the Northern Hemisphere, a harsh flu season leading to more sick leave, and holidays arriving early on the calendar.(7)

Growth forecasts for the key Asia-Pacific economies still look bright. As an example, take the Asian Development Bank’s projections. The ADB sees economic expansion of 7.3% in India this year, 6.6% growth in China, better than 5% growth in Malaysia, and Thailand’s economy developing at better than 4%. It did cite tariffs as a risk, but emphasized that they had yet to affect trade. Speaking of tariffs and trade, the E.U. requested a permanent exemption from U.S. import tariffs as May began. It has threatened to levy taxes on €2.8 billion of U.S. exports if the Trump administration’s planned excise taxes take effect.(8,9)

WORLD MARKETS

Look at these gains by benchmarks overseas, which far exceed those of our major stock indices in April: Nikkei 225, 6.83%; CAC 40, 6.84%; BSE Sensex, 6.65%; FTSE 100, 6.42%; Nifty 50, 6.19%; DAX, 4.26%; FTSE Eurofirst 300, 4.11%; IBEX 35, 3.96%. To our south, Mexico’s Bolsa rose 4.84% last month.(10)

These were not the only significant advances. Australia’s All Ordinaries improved 3.45%; South Korea’s Kospi, 2.84%. Canada’s TSX Composite added 1.57%. MSCI’s World index rose 0.95% in April. There were also some April setbacks. MSCI’s Emerging Markets index fell 0.55%, China’s Shanghai Composite took a 2.67% loss, Taiwan’s TSE 50 slipped 3.24%, and Argentina’s Merval retreated 3.56%.(10,11)

COMMODITIES MARKETS

Two crops recorded the biggest gains among major commodity futures in April. Wheat jumped 14.11%, and cocoa soared 11.13%. WTI crude also rose conspicuously, gaining 5.61% and finishing the month at $68.54 on the NYMEX. Heating oil and unleaded gasoline performed even better than crude, respectively adding 6.27% and 5.94% for April. Other solid gains came for cotton, which rose 3.74%; coffee, which improved 1.86%; natural gas, up 1.35%. Two soft commodities did retreat: sugar slipped 2.35%; soybeans, 0.57%.(12)

A dollar rally meant a 1.59% advance for the U.S. Dollar Index last month; it closed at 91.58 on April 30. Metals were mixed: copper rose 1.03%, and silver ascended 0.46%, but gold declined 0.63% in April, and platinum lost 2.36%. Gold ended April at $1,316.70 on the COMEX; silver, at $16.36.(12,13)

REAL ESTATE

The March home buying numbers were positive. Existing home sales improved 1.1% as inventory finally grew a bit (there was still just 3.6 months of supply available). The median sale price of an existing home rose to $250,400. Resales were still down 1.2% year-over-year, according to the National Association of Realtors. New home buying rose 4.0% in March, the Census Bureau stated; that took them to a 4-month high and put the year-over-year sales gain at 8.8%, with the median sale price up 4.8% in 12 months.(14,15)

Perhaps buyers were eager to try and lock in lower mortgage rates while they could. The rise in mean mortgage rates in April was striking. Freddie Mac’s Primary Mortgage Market Surveys from April 26 and March 29 show the size of the increases. On April 26, the average interest rates on common home loan types were as follows: 30-year fixed, 4.58%; 15-year fixed, 4.02%; 5/1-year adjustable, 3.74%. Look at the numbers from March 29: 30-year FRM, 4.44%; 15-year FRM, 3.90%; 5/1-year ARM, 3.66%.(16)

The latest S&P CoreLogic Case-Shiller house price index recorded a 6.3% annual advance through February, exceeding the 6.1% year-over-year gain of a month before. Groundbreaking increased 1.9% in March and building permits rose 2.5%; in February, both indicators were in the red. The NAR’s pending home sales index rose 0.4% for March.(3,4)

LOOKING BACK…LOOKING FORWARD

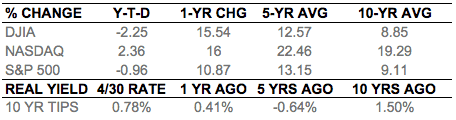

At the end of April, the major indices were not far removed from where they were at the start of the month. The S&P 500 added just 0.27%; the Dow Jones Industrial Average 0.25%. The Nasdaq Composite managed a meager 0.04% advance. These minor gains led the big three to the following April 30 settlements: DJIA, 24,163.15; COMP, 7,066.27; S&P, 2,648.05. Small caps had a decent month: the Russell 2000 improved 0.81% to 1,541.88. The CBOE VIX “fear index” ended the month at 15.93, diving 20.23%. The NYSE Arca Biotech Index was up 5.98% YTD through April.(1,17)

Indices are unmanaged, do not incur fees or expenses, and cannot be invested into directly. These returns do not include dividends. 10-year TIPS real yield = projected return at maturity given expected inflation.

Will investors “sell in May and go away” in 2018 when they have already been selling? Maybe not. Over the last 20 years, the S&P 500 has advanced 70% of the time during May-October, with the mean gain being 1.2% across those six months. Who knows, perhaps greater spring and summer gains than that await. Mid-term elections are ahead, though, and since 1950, the average May-October return for the S&P 500 has been nearly flat in such years. Consider all this history with a few grains of salt, as the past cannot predict future performance. What happens with tariffs, trade pacts, and Syria and North Korea could influence investors enormously in May. In fact, those developments could even set a tone for the market across the next few months. Investors may proceed cautiously this month as they wait for uncertainties to resolve.(21)

UPCOMING ECONOMIC RELEASES: Across the rest of May, the important news items include: the April employment report from the Department of Labor (5/4), a new Producer Price Index (5/9), the latest Consumer Price Index (5/10), the University of Michigan’s preliminary May consumer sentiment index (5/11), April retail sales (5/15), April housing starts, building permits, and industrial output (5/16), the Conference Board’s April index of leading indicators (5/17), April new home sales (5/23), April existing home sales (5/24), April hard goods orders and the final May University of Michigan consumer sentiment index (5/25), the May Conference Board consumer confidence index (5/29), a second estimate of Q1 GDP from the Bureau of Economic Analysis and the May ADP payrolls report (5/30), and lastly, April pending home sales, April consumer spending, and the latest PCE price index (5/31).

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. The information herein has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. Investments will fluctuate and when redeemed may be worth more or less than when originally invested. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All market indices discussed are unmanaged and are not illustrative of any particular investment. Indices do not incur management fees, costs and expenses, and cannot be invested into directly. All economic and performance data is historical and not indicative of future results. The Dow Jones Industrial Average is a price-weighted index of 30 actively traded blue-chip stocks. The NASDAQ Composite Index is a market-weighted index of all over-the-counter common stocks traded on the National Association of Securities Dealers Automated Quotation System. The Standard & Poor’s 500 (S&P 500) is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy. The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. The CBOE Volatility Index® (VIX®) is a key measure of market expectations of near-term volatility conveyed by S&P 500 stock index option prices. NYSE Group, Inc. (NYSE:NYX) operates two securities exchanges: the New York Stock Exchange (the “NYSE”) and NYSE Arca (formerly known as the Archipelago Exchange, or ArcaEx®, and the Pacific Exchange). NYSE Group is a leading provider of securities listing, trading and market data products and services. The New York Mercantile Exchange, Inc. (NYMEX) is the world’s largest physical commodity futures exchange and the preeminent trading forum for energy and precious metals, with trading conducted through two divisions – the NYMEX Division, home to the energy, platinum, and palladium markets, and the COMEX Division, on which all other metals trade. Nikkei 225 (Ticker: ^N225) is a stock market index for the Tokyo Stock Exchange (TSE). The Nikkei average is the most watched index of Asian stocks. The CAC-40 Index is a narrow-based, modified capitalization-weighted index of 40 companies listed on the Paris Bourse. The BSE SENSEX (Bombay Stock Exchange Sensitive Index), also-called the BSE 30 (BOMBAY STOCK EXCHANGE) or simply the SENSEX, is a free-float market capitalization-weighted stock market index of 30 well-established and financially sound companies listed on the Bombay Stock Exchange (BSE). The FTSE 100 Index is a share index of the 100 companies listed on the London Stock Exchange with the highest market capitalization. The Nifty 50 (NTFE 50) is a well-diversified 50-stock index accounting for 13 sectors of the Indian economy. It is used for a variety of purposes such as benchmarking fund portfolios, index-based derivatives and index funds. The DAX 30 is a Blue-Chip stock market index consisting of the 30 major German companies trading on the Frankfurt Stock Exchange. The FTSEurofirst 300 Index comprises the 300 largest companies ranked by market capitalisation in the FTSE Developed Europe Index. The IBEX 35 is the benchmark stock market index of the Bolsa de Madrid, Spain’s principal stock exchange. The Mexican Stock Exchange, commonly known as Mexican Bolsa, Mexbol, or BMV, is the only stock exchange in Mexico. The All Ordinaries (XAO) is considered a total market barometer for the Australian stock market and contains the 500 largest ASX-listed companies by way of market capitalization. The Korea Composite Stock Price Index or KOSPI is the major stock market index of South Korea, representing all common stocks traded on the Korea Exchange. The S&P/TSX Composite Index is an index of the stock (equity) prices of the largest companies on the Toronto Stock Exchange (TSX) as measured by market capitalization. The MSCI World Index is a free-float weighted equity index that includes developed world markets, and does not include emerging markets. The MSCI Emerging Markets Index is a float-adjusted market capitalization index consisting of indices in more than 25 emerging economies. The SSE Composite Index is an index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange. The FTSE TWSE Taiwan 50 Index consists of the largest 50 companies by full market value, and is also the first narrow-based index published in Taiwan. The MERVAL Index (MERcado de VALores, literally Stock Exchange) is the most important index of the Buenos Aires Stock Exchange. The US Dollar Index measures the performance of the U.S. dollar against a basket of six currencies. The NYSE Arca Biotechnology IndexSM is an equal dollar weighted index designed to measure the performance of a cross section of companies in the biotechnology industry that are primarily involved in the use of biological processes to develop products or provide services. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. MarketingPro, Inc. is not affiliated with any person or firm that may be providing this information to you. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional.

Citations.

1 – quotes.wsj.com/index/SPX [4/30/18]

2 – tinyurl.com/yc9x6klv [4/30/18]

3 – marketwatch.com/economy-politics/calendars/economic [5/1/18]

4 – investing.com/economic-calendar/ [5/1/18]

5 – tinyurl.com/ydhcz6fz [3/30/18]

6 – instituteforsupplymanagement.org/ISMReport/NonMfgROB.cfm?SSO=1 [4/4/18]

7 – reuters.com/article/us-global-economy-data-analysis/peak-or-pause-global-economys-hesitation-unnerves-markets-idUSKBN1HW21J [4/25/18]

8 – tinyurl.com/y839l9hx [4/11/18]

9 – reuters.com/article/us-usa-trade-metals-eu/eu-says-trump-tariff-uncertainty-is-hitting-business-idUSKBN1I22X3 [5/1/18]

10 – markets.on.nytimes.com/research/markets/worldmarkets/worldmarkets.asp [4/30/18]

11 – msci.com/end-of-day-data-search [4/30/18]

12 – money.cnn.com/data/commodities/ [4/30/18]

13 – marketwatch.com/investing/index/dxy/historical [4/30/18]

14 – tradingeconomics.com/united-states/existing-home-sales [5/1/18]

15 – marketwatch.com/story/new-home-sales-roar-to-a-4-month-high-in-march-2018-04-24 [4/24/18]

16 – freddiemac.com/pmms/archive.html [4/30/18]

17 – markets.wsj.com/us [4/30/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=5%2F1%2F17&x=0&y=0 [4/30/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=5%2F1%2F17&x=0&y=0 [4/30/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=5%2F1%2F17&x=0&y=0 [4/30/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=4%2F30%2F13&x=0&y=0 [4/30/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=4%2F30%2F13&x=0&y=0 [4/30/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=4%2F30%2F13&x=0&y=0 [4/30/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=4%2F30%2F08&x=0&y=0 [4/30/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=4%2F30%2F08&x=0&y=0 [4/30/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=4%2F30%2F08&x=0&y=0 [4/30/18]

19 – treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyieldYear&year=2018 [4/30/18]

20 – treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyieldAll [4/30/18]

21 – cnbc.com/2018/04/30/why-investors-may-not-want-to-sell-in-may-this-year.html [4/30/18]

THE MONTH IN BRIEF

April saw the S&P 500 advance 0.27% as a new earnings season unfolded – one in which investors grew uneasy about rising Treasury yields, protectionism, and privacy concerns involving tech giants. While the financial media largely focused on those anxieties, good news also appeared. The latest consumer spending and consumer confidence data was solid. Home buying picked up as listings increased slightly. Oil rallied, and so did the dollar. Overseas equity benchmarks saw big gains, even as some economists wondered if the boom in global growth was fading. One of the major financial news stories of April broke only hours before the start of May: a postponement of the tariffs planned for imported metals.(1)

DOMESTIC ECONOMIC HEALTH

On the night of April 30, the Trump administration elected to delay the imposition of excise taxes on aluminum and steel imported to America from China, Mexico, Canada, Brazil, Argentina, Australia, and the European Union. Those tariffs were set to take effect on May 1, but they are now on hold until at least June 1 (2)

Consumer spending was strong in March, according to the Department of Commerce. Households devoted 0.4% more of their incomes to consumer purchases than they did in February (and household incomes rose 0.3%). Retail sales picked up 0.6% in March, quite a change from the 0.1% decline in February. The Bureau of Economic Analysis released its first estimate of first quarter GDP in late April: 2.3%.(3)

Consumer confidence indices ended the month on an upswing. The University of Michigan’s index had a final April reading of 98.8, a point higher than its initial April mark. The Conference Board’s index came in at 128.7, a rise of 1.7 points from March; it surpassed MarketWatch’s consensus forecast by 2.8 points.(3)

Inflation pressure was mounting: the year-over-year change in the Consumer Price Index was 2.4% through March, even with a 0.1% retreat for the headline CPI. (That compares to 2.2% annualized inflation in February.) The core CPI was up 2.1% in the 12 months ending in March, compared to a yearly gain of 1.8% a month previously. Annual wholesale inflation reached 3.0% as the first quarter ended. The March employment report from the Department of Labor showed wages keeping pace with consumer costs; they were rising at 2.7% annually.(4,5)

The rest of the March jobs report was disappointing. Employers added only 103,000 net new hires, the lowest monthly total in half a year. Some economists thought weather held hiring back in certain industries. The Department of Labor recorded unemployment at 4.1% for a sixth consecutive month; the good news was the 0.2% dip in the U-6 jobless rate that encompasses underemployed Americans. In March, the U-6 rate fell to 8.0%.(5)

Once again, expansion in the manufacturing and service industries impressed. The Institute for Supply Management’s twin purchasing manager indices were in the high fifties in March; they both declined from lofty February readings. ISM’s factory PMI descended to 59.3 in March from 60.8 and wound up at 57.3 in April. Its service sector PMI fell from 59.5 to 58.8 in March. Durable goods orders rose 2.6% for March.(3,6)

GLOBAL ECONOMIC HEALTH

Were seemingly healthy economies in Europe losing momentum? Investors, economists, and journalists noticed some deterioration in fundamentals. An index of German business confidence touched a low unseen in a year in April, echoing a drop in a broader eurozone index. Markit’s eurozone manufacturing PMI was 56.0 at last reading, but about five points lower than its late 2017 peak. The Baltic Dry Freight Index, a barometer of shipping activity, fell to an 8-month low in April. The yield curve for government bonds has been flattening in western economies, a signal of more pessimism than optimism. Still, some analysts call these declines seasonal, reflective of rough weather in the Northern Hemisphere, a harsh flu season leading to more sick leave, and holidays arriving early on the calendar.(7)

Growth forecasts for the key Asia-Pacific economies still look bright. As an example, take the Asian Development Bank’s projections. The ADB sees economic expansion of 7.3% in India this year, 6.6% growth in China, better than 5% growth in Malaysia, and Thailand’s economy developing at better than 4%. It did cite tariffs as a risk, but emphasized that they had yet to affect trade. Speaking of tariffs and trade, the E.U. requested a permanent exemption from U.S. import tariffs as May began. It has threatened to levy taxes on €2.8 billion of U.S. exports if the Trump administration’s planned excise taxes take effect.(8,9)

WORLD MARKETS

Look at these gains by benchmarks overseas, which far exceed those of our major stock indices in April: Nikkei 225, 6.83%; CAC 40, 6.84%; BSE Sensex, 6.65%; FTSE 100, 6.42%; Nifty 50, 6.19%; DAX, 4.26%; FTSE Eurofirst 300, 4.11%; IBEX 35, 3.96%. To our south, Mexico’s Bolsa rose 4.84% last month.(10)

These were not the only significant advances. Australia’s All Ordinaries improved 3.45%; South Korea’s Kospi, 2.84%. Canada’s TSX Composite added 1.57%. MSCI’s World index rose 0.95% in April. There were also some April setbacks. MSCI’s Emerging Markets index fell 0.55%, China’s Shanghai Composite took a 2.67% loss, Taiwan’s TSE 50 slipped 3.24%, and Argentina’s Merval retreated 3.56%.(10,11)

COMMODITIES MARKETS

Two crops recorded the biggest gains among major commodity futures in April. Wheat jumped 14.11%, and cocoa soared 11.13%. WTI crude also rose conspicuously, gaining 5.61% and finishing the month at $68.54 on the NYMEX. Heating oil and unleaded gasoline performed even better than crude, respectively adding 6.27% and 5.94% for April. Other solid gains came for cotton, which rose 3.74%; coffee, which improved 1.86%; natural gas, up 1.35%. Two soft commodities did retreat: sugar slipped 2.35%; soybeans, 0.57%.(12)

A dollar rally meant a 1.59% advance for the U.S. Dollar Index last month; it closed at 91.58 on April 30. Metals were mixed: copper rose 1.03%, and silver ascended 0.46%, but gold declined 0.63% in April, and platinum lost 2.36%. Gold ended April at $1,316.70 on the COMEX; silver, at $16.36.(12,13)

REAL ESTATE

The March home buying numbers were positive. Existing home sales improved 1.1% as inventory finally grew a bit (there was still just 3.6 months of supply available). The median sale price of an existing home rose to $250,400. Resales were still down 1.2% year-over-year, according to the National Association of Realtors. New home buying rose 4.0% in March, the Census Bureau stated; that took them to a 4-month high and put the year-over-year sales gain at 8.8%, with the median sale price up 4.8% in 12 months.(14,15)

Perhaps buyers were eager to try and lock in lower mortgage rates while they could. The rise in mean mortgage rates in April was striking. Freddie Mac’s Primary Mortgage Market Surveys from April 26 and March 29 show the size of the increases. On April 26, the average interest rates on common home loan types were as follows: 30-year fixed, 4.58%; 15-year fixed, 4.02%; 5/1-year adjustable, 3.74%. Look at the numbers from March 29: 30-year FRM, 4.44%; 15-year FRM, 3.90%; 5/1-year ARM, 3.66%.(16)

The latest S&P CoreLogic Case-Shiller house price index recorded a 6.3% annual advance through February, exceeding the 6.1% year-over-year gain of a month before. Groundbreaking increased 1.9% in March and building permits rose 2.5%; in February, both indicators were in the red. The NAR’s pending home sales index rose 0.4% for March.(3,4)

LOOKING BACK…LOOKING FORWARD

At the end of April, the major indices were not far removed from where they were at the start of the month. The S&P 500 added just 0.27%; the Dow Jones Industrial Average 0.25%. The Nasdaq Composite managed a meager 0.04% advance. These minor gains led the big three to the following April 30 settlements: DJIA, 24,163.15; COMP, 7,066.27; S&P, 2,648.05. Small caps had a decent month: the Russell 2000 improved 0.81% to 1,541.88. The CBOE VIX “fear index” ended the month at 15.93, diving 20.23%. The NYSE Arca Biotech Index was up 5.98% YTD through April.(1,17)

Indices are unmanaged, do not incur fees or expenses, and cannot be invested into directly. These returns do not include dividends. 10-year TIPS real yield = projected return at maturity given expected inflation.

Will investors “sell in May and go away” in 2018 when they have already been selling? Maybe not. Over the last 20 years, the S&P 500 has advanced 70% of the time during May-October, with the mean gain being 1.2% across those six months. Who knows, perhaps greater spring and summer gains than that await. Mid-term elections are ahead, though, and since 1950, the average May-October return for the S&P 500 has been nearly flat in such years. Consider all this history with a few grains of salt, as the past cannot predict future performance. What happens with tariffs, trade pacts, and Syria and North Korea could influence investors enormously in May. In fact, those developments could even set a tone for the market across the next few months. Investors may proceed cautiously this month as they wait for uncertainties to resolve.(21)

UPCOMING ECONOMIC RELEASES: Across the rest of May, the important news items include: the April employment report from the Department of Labor (5/4), a new Producer Price Index (5/9), the latest Consumer Price Index (5/10), the University of Michigan’s preliminary May consumer sentiment index (5/11), April retail sales (5/15), April housing starts, building permits, and industrial output (5/16), the Conference Board’s April index of leading indicators (5/17), April new home sales (5/23), April existing home sales (5/24), April hard goods orders and the final May University of Michigan consumer sentiment index (5/25), the May Conference Board consumer confidence index (5/29), a second estimate of Q1 GDP from the Bureau of Economic Analysis and the May ADP payrolls report (5/30), and lastly, April pending home sales, April consumer spending, and the latest PCE price index (5/31).

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. The information herein has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. Investments will fluctuate and when redeemed may be worth more or less than when originally invested. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All market indices discussed are unmanaged and are not illustrative of any particular investment. Indices do not incur management fees, costs and expenses, and cannot be invested into directly. All economic and performance data is historical and not indicative of future results. The Dow Jones Industrial Average is a price-weighted index of 30 actively traded blue-chip stocks. The NASDAQ Composite Index is a market-weighted index of all over-the-counter common stocks traded on the National Association of Securities Dealers Automated Quotation System. The Standard & Poor’s 500 (S&P 500) is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy. The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. The CBOE Volatility Index® (VIX®) is a key measure of market expectations of near-term volatility conveyed by S&P 500 stock index option prices. NYSE Group, Inc. (NYSE:NYX) operates two securities exchanges: the New York Stock Exchange (the “NYSE”) and NYSE Arca (formerly known as the Archipelago Exchange, or ArcaEx®, and the Pacific Exchange). NYSE Group is a leading provider of securities listing, trading and market data products and services. The New York Mercantile Exchange, Inc. (NYMEX) is the world’s largest physical commodity futures exchange and the preeminent trading forum for energy and precious metals, with trading conducted through two divisions – the NYMEX Division, home to the energy, platinum, and palladium markets, and the COMEX Division, on which all other metals trade. Nikkei 225 (Ticker: ^N225) is a stock market index for the Tokyo Stock Exchange (TSE). The Nikkei average is the most watched index of Asian stocks. The CAC-40 Index is a narrow-based, modified capitalization-weighted index of 40 companies listed on the Paris Bourse. The BSE SENSEX (Bombay Stock Exchange Sensitive Index), also-called the BSE 30 (BOMBAY STOCK EXCHANGE) or simply the SENSEX, is a free-float market capitalization-weighted stock market index of 30 well-established and financially sound companies listed on the Bombay Stock Exchange (BSE). The FTSE 100 Index is a share index of the 100 companies listed on the London Stock Exchange with the highest market capitalization. The Nifty 50 (NTFE 50) is a well-diversified 50-stock index accounting for 13 sectors of the Indian economy. It is used for a variety of purposes such as benchmarking fund portfolios, index-based derivatives and index funds. The DAX 30 is a Blue-Chip stock market index consisting of the 30 major German companies trading on the Frankfurt Stock Exchange. The FTSEurofirst 300 Index comprises the 300 largest companies ranked by market capitalisation in the FTSE Developed Europe Index. The IBEX 35 is the benchmark stock market index of the Bolsa de Madrid, Spain’s principal stock exchange. The Mexican Stock Exchange, commonly known as Mexican Bolsa, Mexbol, or BMV, is the only stock exchange in Mexico. The All Ordinaries (XAO) is considered a total market barometer for the Australian stock market and contains the 500 largest ASX-listed companies by way of market capitalization. The Korea Composite Stock Price Index or KOSPI is the major stock market index of South Korea, representing all common stocks traded on the Korea Exchange. The S&P/TSX Composite Index is an index of the stock (equity) prices of the largest companies on the Toronto Stock Exchange (TSX) as measured by market capitalization. The MSCI World Index is a free-float weighted equity index that includes developed world markets, and does not include emerging markets. The MSCI Emerging Markets Index is a float-adjusted market capitalization index consisting of indices in more than 25 emerging economies. The SSE Composite Index is an index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange. The FTSE TWSE Taiwan 50 Index consists of the largest 50 companies by full market value, and is also the first narrow-based index published in Taiwan. The MERVAL Index (MERcado de VALores, literally Stock Exchange) is the most important index of the Buenos Aires Stock Exchange. The US Dollar Index measures the performance of the U.S. dollar against a basket of six currencies. The NYSE Arca Biotechnology IndexSM is an equal dollar weighted index designed to measure the performance of a cross section of companies in the biotechnology industry that are primarily involved in the use of biological processes to develop products or provide services. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. MarketingPro, Inc. is not affiliated with any person or firm that may be providing this information to you. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional.

Citations.

1 – quotes.wsj.com/index/SPX [4/30/18]

2 – tinyurl.com/yc9x6klv [4/30/18]

3 – marketwatch.com/economy-politics/calendars/economic [5/1/18]

4 – investing.com/economic-calendar/ [5/1/18]

5 – tinyurl.com/ydhcz6fz [3/30/18]

6 – instituteforsupplymanagement.org/ISMReport/NonMfgROB.cfm?SSO=1 [4/4/18]

7 – reuters.com/article/us-global-economy-data-analysis/peak-or-pause-global-economys-hesitation-unnerves-markets-idUSKBN1HW21J [4/25/18]

8 – tinyurl.com/y839l9hx [4/11/18]

9 – reuters.com/article/us-usa-trade-metals-eu/eu-says-trump-tariff-uncertainty-is-hitting-business-idUSKBN1I22X3 [5/1/18]

10 – markets.on.nytimes.com/research/markets/worldmarkets/worldmarkets.asp [4/30/18]

11 – msci.com/end-of-day-data-search [4/30/18]

12 – money.cnn.com/data/commodities/ [4/30/18]

13 – marketwatch.com/investing/index/dxy/historical [4/30/18]

14 – tradingeconomics.com/united-states/existing-home-sales [5/1/18]

15 – marketwatch.com/story/new-home-sales-roar-to-a-4-month-high-in-march-2018-04-24 [4/24/18]

16 – freddiemac.com/pmms/archive.html [4/30/18]

17 – markets.wsj.com/us [4/30/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=5%2F1%2F17&x=0&y=0 [4/30/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=5%2F1%2F17&x=0&y=0 [4/30/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=5%2F1%2F17&x=0&y=0 [4/30/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=4%2F30%2F13&x=0&y=0 [4/30/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=4%2F30%2F13&x=0&y=0 [4/30/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=4%2F30%2F13&x=0&y=0 [4/30/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=4%2F30%2F08&x=0&y=0 [4/30/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=4%2F30%2F08&x=0&y=0 [4/30/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=4%2F30%2F08&x=0&y=0 [4/30/18]

19 – treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyieldYear&year=2018 [4/30/18]

20 – treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyieldAll [4/30/18]

21 – cnbc.com/2018/04/30/why-investors-may-not-want-to-sell-in-may-this-year.html [4/30/18]