MONTHLY QUOTE

“Never apologize for showing feeling. When you do so, you apologize for truth.”

– Benjamin Disraeli

MONTHLY TIP

Personal finance apps have come a long way. Besides bill paying, account overviews, and push notifications regarding household budget categories, some let you see all your credit and bank transactions in one view. If you have not previously used one, consider one for 2018.

MONTHLY RIDDLE

Sometimes it is good, sometimes it is bad, sometimes you wait for it, other times you fear it. At times you may make it, or even spread it. What is it?

Last month’s riddle

Suzy and Ben stand upon a 200-foot cliff. They both slip down the cliff to the rocks below, but they have dinner together the next day. How can this be?

Last month’s answer:

They rappelled down the cliff.

THE MONTH IN BRIEF

Bulls took charge of Wall Street as 2018 began: the Dow Jones Industrial Average rose 5.79% in the first month of the year, even with a mild selloff on the verge of February. Foreign equity benchmarks largely advanced as well. Oil and gasoline futures surged, while bitcoin continued to rollercoaster. Personal spending, manufacturing, and consumer confidence data encouraged investors. Home sales weakened as home prices surpassed a pre-recession peak and mortgage rates increased. Analysts kept warning that Wall Street was overdue for a pullback; while indices did slip late in the month, optimism was little shaken.1(1)

DOMESTIC ECONOMIC HEALTH

CAmerica’s economy is largely driven by the consumer, and as the Bureau of Economic Analysis noted, consumers spent generously in December. There were 0.4% improvements in both personal income and personal spending. Retail sales rose by 0.4% in the last month of 2017, even with vehicle and gasoline purchases factored out. The BEA released its first estimate of fourth-quarter GDP in late January – a respectable 2.6%.(2)

Consumer confidence index readings varied from extremely impressive to above average. The Conference Board’s monthly index rose from 123.1 to 125.4 in January. In contrast, the University of Michigan’s gauge of consumer sentiment weakened from a final December mark of 95.9 to 94.4. (It was four points higher a year earlier.)(2,3)

Businesses hired 148,000 more workers than they let go in December, a figure which disappointed many analysts. Hourly wage growth remained at 2.5%. Unemployment held at 4.1%, with the U-6 rate including the underemployed rising 0.1% to 8.1%. After revisions to November and October numbers, the Department of Labor calculated average monthly job gains of 204,000 in the final quarter of 2017.(4)

Investors concerned about any weakness in the labor market could find something to cheer about in manufacturing. The Institute for Supply Management’s December purchasing manager index for the U.S. factory sector rose 1.5 points to an impressive reading of 59.7; that PMI dipped to 59.1 in January, which was nonetheless another fine reading. ISM’s non-manufacturing PMI went the other way, losing 1.5 points in December to a still-noteworthy mark of 55.9.(2)

Just when inflation seemed to be accelerating, it slowed again – at least by the assessment of the latest Consumer and Producer Price Indexes. December’s headline CPI showed a 2.1% annualized gain for consumer prices, compared to 2.2% a month earlier. The core CPI showed a 1.8% yearly advance. Prices ticked up 0.1% in the last month of 2017; core prices, 0.3%. Yearly wholesale inflation had reached 3.1% in November; it dropped to 2.6% in December.(2)

Did these inflation numbers threaten to make things difficult for the Federal Reserve as it contemplated its next rate increase? Apparently not. On January 31, the Federal Open Market Committee held rates steady (as anticipated) while noting its expectation that inflation should increase in 2018 and that the economy should “warrant further gradual increases” in the federal funds rate. (Some investors took that as a hint of a March rate move.) This was the FOMC’s last meeting with Janet Yellen as chair.(2,5)

GLOBAL ECONOMIC HEALTH

In 2017, the economy of the European Union reached a peak unseen in more than a decade and outpaced that of the United States. Fresh data from Eurostat showed E.U. GDP of 2.5% for 2017, compared with 2.3% for America. The United Kingdom’s economy lagged, expanding 1.8% in the first full year after the Brexit decision and marking the poorest economic year for the U.K. since 2012. Continental leaders grew concerned last month with the political climate of Italy, the third-largest E.U. economy (and a stagnant one at that). A national election is set for March 4, and the fear is that a shift in political coalitions could prompt anti-establishment leaders to the forefront. In the worst-case scenario, Italy leaves the E.U., a decision which could threaten to wreck the eurozone.(6,7)

According to the latest official data from China, the P.R.C.’s economy grew 6.9% in 2017 – its best showing in seven years, surpassing the government target of 6.5%. (Some analysts believe the nation’s GDP number is regularly inflated and contend that China’s true yearly economic growth is 5% or less.) The private-sector Caixin/Markit factory PMI for China remained at a decent 51.5 in January, even as export orders fell slightly. Japan’s Markit/Nikkei factory PMI reached a four-year high last month, South Korea’s went back over the 50 mark (indicating expansion), and Taiwan’s reached its highest level since April 2011.(8,9)

WORLD MARKETS

A trio of notable equity benchmarks gained more than 10% in January: Argentina’s Merval rose 16.21%; Brazil’s Bovespa, 11.14%; Hong Kong’s Hang Seng, 10.13%. Six more posted monthly increases of between 5-10%: Russia’s Micex added 8.54%; the MSCI Emerging Markets, 8.30%; Taiwan’s TSE 50, 6.32%; India’s Sensex, 5.60%; the Shanghai Composite, 5.25%; MSCI’s World index, 5.22%.(10,11)

More gains to note: India’s Nifty 50, 4.72%; South Korea’s Kospi, 4.13%; Spain’s IBEX 35, 4.06%; France’s CAC 40, 3.19%; Nikkei 225, 2.52%; Mexico’s Bolsa, 2.23%; Germany’s DAX, 2.10%; FTSE Eurofirst 300, 1.60%. Lastly, two benchmarks lost ground last month: Canada’s TSX Composite, which declined 1.59%, and the United Kingdom’s FTSE 100, which dipped 2.01%.(10)

COMMODITIES MARKETS

Many commodities posted January advances; bitcoin was not one of them. The digital currency began January at $13,412.44, but it sat at $10,058.10 at the close on January 31. That descent represented a 25.01% loss. The U.S. Dollar Index lost 3.18% for the month, settling January 31 at 89.19.(12,13)

Light sweet crude ended January at $64.77 per barrel, up 7.77% for the month. Unleaded gasoline rose 5.78%. The news was also good for some other soft commodities: wheat gained 5.68%; cocoa, 5.30%; soybeans, 4.62%; corn, 2.99%. Sugar had it worst, falling 9.50%; coffee fell 3.33%, while cotton lost 2.03%. Heating oil (-0.12%) and natural gas (+0.10%) were little changed.(14)

Platinum led the four key metals in January with a gain of 8.21%, and copper trailed with a 2.59% loss. Gold rose 3.22% and silver, 1.58%; gold ended January at $1,344.40 an ounce, silver at $17.32 an ounce.(14)

REAL ESTATE

The housing market felt a chill in December. Resales declined 3.6% according to the National Association of Realtors, and new home buying weakened 9.3% by the estimation of the Census Bureau.(2)

Harsh weather was not the only factor in the winter sales slowdown. The 20-city S&P CoreLogic Case-Shiller index showed home prices up 6.2% year-over-year through November; moreover, as 2017 ended, existing home values were 6% above where they had been back in 2006.(15)

Mortgage rates climbed steadily in January, adding to affordability concerns and making some real estate analysts wonder if home prices might level off a bit. Freddie Mac’s Primary Mortgage Market Survey provides a quick illustration. On January 25, it found the mean interest rate on the 30-year fixed at 4.15% – just a touch higher than in late January 2017, but up from 3.99% on December 28. In the same time frame, the average interest rate for the 15-year fixed went from 3.44% to 3.62%, while the mean interest on the 5-year adjustable home loan rose from 3.47% to 3.52%.(16,17)

Developers had begun fewer projects in December. In mid-January, the Census Bureau announced an 8.2% drop in housing starts in the preceding month, with building permits down just 0.1%. Lastly, the NAR pending home sales index rose 0.5% in the final month of 2017.(2)

LOOKING BACK…LOOKING FORWARD

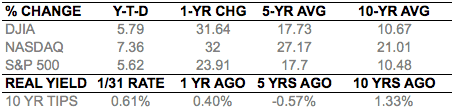

One Wall Street benchmark gained more than twice as much as the S&P 500 in January. The NYSE Arca Biotechnology index jumped 13.01% last month, getting a major lift from the earnings season.(1)

The big three had a great month, as demonstrated by the year-to-date gains shown below. Their January 31 settlements: Dow, 26,149.39; Nasdaq, 7,411.48; S&P 500, 2,823.81. As for the small caps, the Russell 2000 advanced 2.57% year-to-date in January to a month-end close of 1,574.98. Volatility was on the rise: the CBOE VIX gained 22.64% in January to wrap up the month at 13.54.(1)

Indices are unmanaged, do not incur fees or expenses, and cannot be invested into directly. These returns do not include dividends. 10-year TIPS real yield = projected return at maturity given expected inflation.

As January ended, the stock market “melt-up” was in full effect: no one wanted to miss out on such amazing gains, and seemingly everyone was running to direct money into equities. During the first few trading days of February, we did not quite see a meltdown, but we did see a stunning pullback, at this writing possibly heralding a correction. The market has been abnormally calm for many months. Expect February to be a month of ups and downs, the types that may give investors pause. The good news is, the economy’s fundamentals are still strong, even as Wall Street worries that rising interest rates may make fixed-income investments more attractive. Seasoned investors will ride through the volatility and keep an eye on the big picture. The bull market is being challenged, but the two factors that often end contribute to end years of Wall Street advances – the downside of a business cycle and rapid tightening by the Federal Reserve – do not yet seem to be at hand. A correction can lead to a healthier and less speculative investment climate.

UPCOMING ECONOMIC RELEASES: The major news items across the balance of February are: the January ISM service sector PMI (2/5), January’s Consumer Price Index and retail sales report (2/14), January wholesale inflation and industrial output (2/15), the Census Bureau’s latest snapshot of housing starts and building permits and the initial February University of Michigan consumer sentiment index (2/16), the NAR’s January existing home sales report (2/21), the Conference Board’s January leading indicator index (2/22), the final February University of Michigan consumer sentiment index (2/23), January new home sales (2/26), the Conference Board’s latest consumer confidence index and January hard goods orders (2/27), and finally the second estimate of Q2 GDP and the NAR’s report on January housing contract activity (2/28). January consumer spending figures and the January PCE price index are slated to appear on March 1.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. The information herein has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. Investments will fluctuate and when redeemed may be worth more or less than when originally invested. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All market indices discussed are unmanaged and are not illustrative of any particular investment. Indices do not incur management fees, costs and expenses, and cannot be invested into directly. All economic and performance data is historical and not indicative of future results. The Dow Jones Industrial Average is a price-weighted index of 30 actively traded blue-chip stocks. The NASDAQ Composite Index is a market-weighted index of all over-the-counter common stocks traded on the National Association of Securities Dealers Automated Quotation System. The Standard & Poor’s 500 (S&P 500) is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy. The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. The CBOE Volatility Index® (VIX®) is a key measure of market expectations of near-term volatility conveyed by S&P 500 stock index option prices. NYSE Group, Inc. (NYSE:NYX) operates two securities exchanges: the New York Stock Exchange (the “NYSE”) and NYSE Arca (formerly known as the Archipelago Exchange, or ArcaEx®, and the Pacific Exchange). NYSE Group is a leading provider of securities listing, trading and market data products and services. The New York Mercantile Exchange, Inc. (NYMEX) is the world’s largest physical commodity futures exchange and the preeminent trading forum for energy and precious metals, with trading conducted through two divisions – the NYMEX Division, home to the energy, platinum, and palladium markets, and the COMEX Division, on which all other metals trade. The MERVAL Index (MERcado de VALores, literally Stock Exchange) is the most important index of the Buenos Aires Stock Exchange. The Bovespa Index is a gross total return index weighted by traded volume & is comprised of the most liquid stocks traded on the Sao Paulo Stock Exchange. The Hang Seng Index is a free float-adjusted market capitalization-weighted stock market index that is the main indicator of the overall market performance in Hong Kong. The MICEX 10 Index is an unweighted price index that tracks the ten most liquid Russian stocks listed on MICEX-RTS in Moscow. The MSCI Emerging Markets Index is a float-adjusted market capitalization index consisting of indices in more than 25 emerging economies. The FTSE TWSE Taiwan 50 Index consists of the largest 50 companies by full market value, and is also the first narrow-based index published in Taiwan. The BSE SENSEX (Bombay Stock Exchange Sensitive Index), also-called the BSE 30 (BOMBAY STOCK EXCHANGE) or simply the SENSEX, is a free-float market capitalization-weighted stock market index of 30 well-established and financially sound companies listed on the Bombay Stock Exchange (BSE). The SSE Composite Index is an index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange. The MSCI World Index is a free-float weighted equity index that includes developed world markets, and does not include emerging markets. The Nifty 50 (NTFE 50) is a well-diversified 50-stock index accounting for 13 sectors of the Indian economy. It is used for a variety of purposes such as benchmarking fund portfolios, index-based derivatives and index funds. The Korea Composite Stock Price Index or KOSPI is the major stock market index of South Korea, representing all common stocks traded on the Korea Exchange. The IBEX 35 is the benchmark stock market index of the Bolsa de Madrid, Spain’s principal stock exchange. The CAC-40 Index is a narrow-based, modified capitalization-weighted index of 40 companies listed on the Paris Bourse. Nikkei 225 (Ticker: ^N225) is a stock market index for the Tokyo Stock Exchange (TSE). The Nikkei average is the most watched index of Asian stocks. The Mexican Stock Exchange, commonly known as Mexican Bolsa, Mexbol, or BMV, is the only stock exchange in Mexico. The DAX 30 is a Blue-Chip stock market index consisting of the 30 major German companies trading on the Frankfurt Stock Exchange. The FTSEurofirst 300 Index comprises the 300 largest companies ranked by market capitalisation in the FTSE Developed Europe Index. The S&P/TSX Composite Index is an index of the stock (equity) prices of the largest companies on the Toronto Stock Exchange (TSX) as measured by market capitalization. The FTSE 100 Index is a share index of the 100 companies listed on the London Stock Exchange with the highest market capitalization. The US Dollar Index measures the performance of the U.S. dollar against a basket of six currencies. The NYSE Arca Biotechnology IndexSM is an equal dollar weighted index designed to measure the performance of a cross section of companies in the biotechnology industry that are primarily involved in the use of biological processes to develop products or provide services. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. MarketingPro, Inc. is not affiliated with any person or firm that may be providing this information to you. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional.

Citations.

1 – markets.wsj.com/us [1/31/18]

2 – investing.com/economic-calendar/ [1/31/18]

3 – sca.isr.umich.edu/ [1/19/18]

4 – forbes.com/sites/maggiemcgrath/2018/01/05/unemployment-rate-holds-steady-at-4-1-as-u-s-adds-148000-jobs-in-december/ [1/5/18]

5 – tinyurl.com/yaq6l5g3 [1/31/18]

6 – euronews.com/2018/01/31/europe-s-economy-grew-faster-than-the-us-in-2017 [1/31/18]

7 – forbes.com/sites/stratfor/2018/01/23/europe-braces-for-the-next-italian-election/ [1/23/18]

8 – reuters.com/article/us-china-economy-gdp/chinas-2017-gdp-growth-accelerates-for-first-time-in-seven-years-idUSKBN1F70OJ [1/18/18]

9 – reuters.com/article/us-global-economy/factories-start-2018-on-solid-footing-idUSKBN1FL51L [2/1/18]

10 – markets.on.nytimes.com/research/markets/worldmarkets/worldmarkets.asp [1/31/18]

11 – msci.com/end-of-day-data-search [1/31/18]

12 – coindesk.com/price/ [1/31/18]

13 – marketwatch.com/investing/index/dxy/historical [1/31/18]

14 – money.cnn.com/data/commodities/ [1/31/18]

15 – cnbc.com/2018/01/30/home-prices-surge-to-new-high-up-6-point-2-percent-in-november.html [1/30/18]

16 – freddiemac.com/pmms/ [1/31/18]

17 – freddiemac.com/pmms/archive.html?year=2017 [1/31/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=1%2F31%2F17&x=0&y=0 [1/31/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=1%2F31%2F17&x=0&y=0 [1/31/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=1%2F31%2F17&x=0&y=0 [1/31/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=1%2F31%2F13&x=0&y=0 [1/31/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=1%2F31%2F13&x=0&y=0 [1/31/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=1%2F31%2F13&x=0&y=0 [1/31/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=1%2F31%2F08&x=0&y=0 [1/31/18]

THE MONTH IN BRIEF

Bulls took charge of Wall Street as 2018 began: the Dow Jones Industrial Average rose 5.79% in the first month of the year, even with a mild selloff on the verge of February. Foreign equity benchmarks largely advanced as well. Oil and gasoline futures surged, while bitcoin continued to rollercoaster. Personal spending, manufacturing, and consumer confidence data encouraged investors. Home sales weakened as home prices surpassed a pre-recession peak and mortgage rates increased. Analysts kept warning that Wall Street was overdue for a pullback; while indices did slip late in the month, optimism was little shaken.1(1)

DOMESTIC ECONOMIC HEALTH

CAmerica’s economy is largely driven by the consumer, and as the Bureau of Economic Analysis noted, consumers spent generously in December. There were 0.4% improvements in both personal income and personal spending. Retail sales rose by 0.4% in the last month of 2017, even with vehicle and gasoline purchases factored out. The BEA released its first estimate of fourth-quarter GDP in late January – a respectable 2.6%.(2)

Consumer confidence index readings varied from extremely impressive to above average. The Conference Board’s monthly index rose from 123.1 to 125.4 in January. In contrast, the University of Michigan’s gauge of consumer sentiment weakened from a final December mark of 95.9 to 94.4. (It was four points higher a year earlier.)(2,3)

Businesses hired 148,000 more workers than they let go in December, a figure which disappointed many analysts. Hourly wage growth remained at 2.5%. Unemployment held at 4.1%, with the U-6 rate including the underemployed rising 0.1% to 8.1%. After revisions to November and October numbers, the Department of Labor calculated average monthly job gains of 204,000 in the final quarter of 2017.(4)

Investors concerned about any weakness in the labor market could find something to cheer about in manufacturing. The Institute for Supply Management’s December purchasing manager index for the U.S. factory sector rose 1.5 points to an impressive reading of 59.7; that PMI dipped to 59.1 in January, which was nonetheless another fine reading. ISM’s non-manufacturing PMI went the other way, losing 1.5 points in December to a still-noteworthy mark of 55.9.(2)

Just when inflation seemed to be accelerating, it slowed again – at least by the assessment of the latest Consumer and Producer Price Indexes. December’s headline CPI showed a 2.1% annualized gain for consumer prices, compared to 2.2% a month earlier. The core CPI showed a 1.8% yearly advance. Prices ticked up 0.1% in the last month of 2017; core prices, 0.3%. Yearly wholesale inflation had reached 3.1% in November; it dropped to 2.6% in December.(2)

Did these inflation numbers threaten to make things difficult for the Federal Reserve as it contemplated its next rate increase? Apparently not. On January 31, the Federal Open Market Committee held rates steady (as anticipated) while noting its expectation that inflation should increase in 2018 and that the economy should “warrant further gradual increases” in the federal funds rate. (Some investors took that as a hint of a March rate move.) This was the FOMC’s last meeting with Janet Yellen as chair.(2,5)

GLOBAL ECONOMIC HEALTH

In 2017, the economy of the European Union reached a peak unseen in more than a decade and outpaced that of the United States. Fresh data from Eurostat showed E.U. GDP of 2.5% for 2017, compared with 2.3% for America. The United Kingdom’s economy lagged, expanding 1.8% in the first full year after the Brexit decision and marking the poorest economic year for the U.K. since 2012. Continental leaders grew concerned last month with the political climate of Italy, the third-largest E.U. economy (and a stagnant one at that). A national election is set for March 4, and the fear is that a shift in political coalitions could prompt anti-establishment leaders to the forefront. In the worst-case scenario, Italy leaves the E.U., a decision which could threaten to wreck the eurozone.(6,7)

According to the latest official data from China, the P.R.C.’s economy grew 6.9% in 2017 – its best showing in seven years, surpassing the government target of 6.5%. (Some analysts believe the nation’s GDP number is regularly inflated and contend that China’s true yearly economic growth is 5% or less.) The private-sector Caixin/Markit factory PMI for China remained at a decent 51.5 in January, even as export orders fell slightly. Japan’s Markit/Nikkei factory PMI reached a four-year high last month, South Korea’s went back over the 50 mark (indicating expansion), and Taiwan’s reached its highest level since April 2011.(8,9)

WORLD MARKETS

A trio of notable equity benchmarks gained more than 10% in January: Argentina’s Merval rose 16.21%; Brazil’s Bovespa, 11.14%; Hong Kong’s Hang Seng, 10.13%. Six more posted monthly increases of between 5-10%: Russia’s Micex added 8.54%; the MSCI Emerging Markets, 8.30%; Taiwan’s TSE 50, 6.32%; India’s Sensex, 5.60%; the Shanghai Composite, 5.25%; MSCI’s World index, 5.22%.(10,11)

More gains to note: India’s Nifty 50, 4.72%; South Korea’s Kospi, 4.13%; Spain’s IBEX 35, 4.06%; France’s CAC 40, 3.19%; Nikkei 225, 2.52%; Mexico’s Bolsa, 2.23%; Germany’s DAX, 2.10%; FTSE Eurofirst 300, 1.60%. Lastly, two benchmarks lost ground last month: Canada’s TSX Composite, which declined 1.59%, and the United Kingdom’s FTSE 100, which dipped 2.01%.(10)

COMMODITIES MARKETS

Many commodities posted January advances; bitcoin was not one of them. The digital currency began January at $13,412.44, but it sat at $10,058.10 at the close on January 31. That descent represented a 25.01% loss. The U.S. Dollar Index lost 3.18% for the month, settling January 31 at 89.19.(12,13)

Light sweet crude ended January at $64.77 per barrel, up 7.77% for the month. Unleaded gasoline rose 5.78%. The news was also good for some other soft commodities: wheat gained 5.68%; cocoa, 5.30%; soybeans, 4.62%; corn, 2.99%. Sugar had it worst, falling 9.50%; coffee fell 3.33%, while cotton lost 2.03%. Heating oil (-0.12%) and natural gas (+0.10%) were little changed.(14)

Platinum led the four key metals in January with a gain of 8.21%, and copper trailed with a 2.59% loss. Gold rose 3.22% and silver, 1.58%; gold ended January at $1,344.40 an ounce, silver at $17.32 an ounce.(14)

REAL ESTATE

The housing market felt a chill in December. Resales declined 3.6% according to the National Association of Realtors, and new home buying weakened 9.3% by the estimation of the Census Bureau.(2)

Harsh weather was not the only factor in the winter sales slowdown. The 20-city S&P CoreLogic Case-Shiller index showed home prices up 6.2% year-over-year through November; moreover, as 2017 ended, existing home values were 6% above where they had been back in 2006.(15)

Mortgage rates climbed steadily in January, adding to affordability concerns and making some real estate analysts wonder if home prices might level off a bit. Freddie Mac’s Primary Mortgage Market Survey provides a quick illustration. On January 25, it found the mean interest rate on the 30-year fixed at 4.15% – just a touch higher than in late January 2017, but up from 3.99% on December 28. In the same time frame, the average interest rate for the 15-year fixed went from 3.44% to 3.62%, while the mean interest on the 5-year adjustable home loan rose from 3.47% to 3.52%.(16,17)

Developers had begun fewer projects in December. In mid-January, the Census Bureau announced an 8.2% drop in housing starts in the preceding month, with building permits down just 0.1%. Lastly, the NAR pending home sales index rose 0.5% in the final month of 2017.(2)

LOOKING BACK…LOOKING FORWARD

One Wall Street benchmark gained more than twice as much as the S&P 500 in January. The NYSE Arca Biotechnology index jumped 13.01% last month, getting a major lift from the earnings season.(1)

The big three had a great month, as demonstrated by the year-to-date gains shown below. Their January 31 settlements: Dow, 26,149.39; Nasdaq, 7,411.48; S&P 500, 2,823.81. As for the small caps, the Russell 2000 advanced 2.57% year-to-date in January to a month-end close of 1,574.98. Volatility was on the rise: the CBOE VIX gained 22.64% in January to wrap up the month at 13.54.(1)

Indices are unmanaged, do not incur fees or expenses, and cannot be invested into directly. These returns do not include dividends. 10-year TIPS real yield = projected return at maturity given expected inflation.

As January ended, the stock market “melt-up” was in full effect: no one wanted to miss out on such amazing gains, and seemingly everyone was running to direct money into equities. During the first few trading days of February, we did not quite see a meltdown, but we did see a stunning pullback, at this writing possibly heralding a correction. The market has been abnormally calm for many months. Expect February to be a month of ups and downs, the types that may give investors pause. The good news is, the economy’s fundamentals are still strong, even as Wall Street worries that rising interest rates may make fixed-income investments more attractive. Seasoned investors will ride through the volatility and keep an eye on the big picture. The bull market is being challenged, but the two factors that often end contribute to end years of Wall Street advances – the downside of a business cycle and rapid tightening by the Federal Reserve – do not yet seem to be at hand. A correction can lead to a healthier and less speculative investment climate.

UPCOMING ECONOMIC RELEASES: The major news items across the balance of February are: the January ISM service sector PMI (2/5), January’s Consumer Price Index and retail sales report (2/14), January wholesale inflation and industrial output (2/15), the Census Bureau’s latest snapshot of housing starts and building permits and the initial February University of Michigan consumer sentiment index (2/16), the NAR’s January existing home sales report (2/21), the Conference Board’s January leading indicator index (2/22), the final February University of Michigan consumer sentiment index (2/23), January new home sales (2/26), the Conference Board’s latest consumer confidence index and January hard goods orders (2/27), and finally the second estimate of Q2 GDP and the NAR’s report on January housing contract activity (2/28). January consumer spending figures and the January PCE price index are slated to appear on March 1.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. The information herein has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. Investments will fluctuate and when redeemed may be worth more or less than when originally invested. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All market indices discussed are unmanaged and are not illustrative of any particular investment. Indices do not incur management fees, costs and expenses, and cannot be invested into directly. All economic and performance data is historical and not indicative of future results. The Dow Jones Industrial Average is a price-weighted index of 30 actively traded blue-chip stocks. The NASDAQ Composite Index is a market-weighted index of all over-the-counter common stocks traded on the National Association of Securities Dealers Automated Quotation System. The Standard & Poor’s 500 (S&P 500) is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy. The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. The CBOE Volatility Index® (VIX®) is a key measure of market expectations of near-term volatility conveyed by S&P 500 stock index option prices. NYSE Group, Inc. (NYSE:NYX) operates two securities exchanges: the New York Stock Exchange (the “NYSE”) and NYSE Arca (formerly known as the Archipelago Exchange, or ArcaEx®, and the Pacific Exchange). NYSE Group is a leading provider of securities listing, trading and market data products and services. The New York Mercantile Exchange, Inc. (NYMEX) is the world’s largest physical commodity futures exchange and the preeminent trading forum for energy and precious metals, with trading conducted through two divisions – the NYMEX Division, home to the energy, platinum, and palladium markets, and the COMEX Division, on which all other metals trade. The MERVAL Index (MERcado de VALores, literally Stock Exchange) is the most important index of the Buenos Aires Stock Exchange. The Bovespa Index is a gross total return index weighted by traded volume & is comprised of the most liquid stocks traded on the Sao Paulo Stock Exchange. The Hang Seng Index is a free float-adjusted market capitalization-weighted stock market index that is the main indicator of the overall market performance in Hong Kong. The MICEX 10 Index is an unweighted price index that tracks the ten most liquid Russian stocks listed on MICEX-RTS in Moscow. The MSCI Emerging Markets Index is a float-adjusted market capitalization index consisting of indices in more than 25 emerging economies. The FTSE TWSE Taiwan 50 Index consists of the largest 50 companies by full market value, and is also the first narrow-based index published in Taiwan. The BSE SENSEX (Bombay Stock Exchange Sensitive Index), also-called the BSE 30 (BOMBAY STOCK EXCHANGE) or simply the SENSEX, is a free-float market capitalization-weighted stock market index of 30 well-established and financially sound companies listed on the Bombay Stock Exchange (BSE). The SSE Composite Index is an index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange. The MSCI World Index is a free-float weighted equity index that includes developed world markets, and does not include emerging markets. The Nifty 50 (NTFE 50) is a well-diversified 50-stock index accounting for 13 sectors of the Indian economy. It is used for a variety of purposes such as benchmarking fund portfolios, index-based derivatives and index funds. The Korea Composite Stock Price Index or KOSPI is the major stock market index of South Korea, representing all common stocks traded on the Korea Exchange. The IBEX 35 is the benchmark stock market index of the Bolsa de Madrid, Spain’s principal stock exchange. The CAC-40 Index is a narrow-based, modified capitalization-weighted index of 40 companies listed on the Paris Bourse. Nikkei 225 (Ticker: ^N225) is a stock market index for the Tokyo Stock Exchange (TSE). The Nikkei average is the most watched index of Asian stocks. The Mexican Stock Exchange, commonly known as Mexican Bolsa, Mexbol, or BMV, is the only stock exchange in Mexico. The DAX 30 is a Blue-Chip stock market index consisting of the 30 major German companies trading on the Frankfurt Stock Exchange. The FTSEurofirst 300 Index comprises the 300 largest companies ranked by market capitalisation in the FTSE Developed Europe Index. The S&P/TSX Composite Index is an index of the stock (equity) prices of the largest companies on the Toronto Stock Exchange (TSX) as measured by market capitalization. The FTSE 100 Index is a share index of the 100 companies listed on the London Stock Exchange with the highest market capitalization. The US Dollar Index measures the performance of the U.S. dollar against a basket of six currencies. The NYSE Arca Biotechnology IndexSM is an equal dollar weighted index designed to measure the performance of a cross section of companies in the biotechnology industry that are primarily involved in the use of biological processes to develop products or provide services. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. MarketingPro, Inc. is not affiliated with any person or firm that may be providing this information to you. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional.

Citations.

1 – markets.wsj.com/us [1/31/18]

2 – investing.com/economic-calendar/ [1/31/18]

3 – sca.isr.umich.edu/ [1/19/18]

4 – forbes.com/sites/maggiemcgrath/2018/01/05/unemployment-rate-holds-steady-at-4-1-as-u-s-adds-148000-jobs-in-december/ [1/5/18]

5 – tinyurl.com/yaq6l5g3 [1/31/18]

6 – euronews.com/2018/01/31/europe-s-economy-grew-faster-than-the-us-in-2017 [1/31/18]

7 – forbes.com/sites/stratfor/2018/01/23/europe-braces-for-the-next-italian-election/ [1/23/18]

8 – reuters.com/article/us-china-economy-gdp/chinas-2017-gdp-growth-accelerates-for-first-time-in-seven-years-idUSKBN1F70OJ [1/18/18]

9 – reuters.com/article/us-global-economy/factories-start-2018-on-solid-footing-idUSKBN1FL51L [2/1/18]

10 – markets.on.nytimes.com/research/markets/worldmarkets/worldmarkets.asp [1/31/18]

11 – msci.com/end-of-day-data-search [1/31/18]

12 – coindesk.com/price/ [1/31/18]

13 – marketwatch.com/investing/index/dxy/historical [1/31/18]

14 – money.cnn.com/data/commodities/ [1/31/18]

15 – cnbc.com/2018/01/30/home-prices-surge-to-new-high-up-6-point-2-percent-in-november.html [1/30/18]

16 – freddiemac.com/pmms/ [1/31/18]

17 – freddiemac.com/pmms/archive.html?year=2017 [1/31/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=1%2F31%2F17&x=0&y=0 [1/31/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=1%2F31%2F17&x=0&y=0 [1/31/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=1%2F31%2F17&x=0&y=0 [1/31/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=1%2F31%2F13&x=0&y=0 [1/31/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=1%2F31%2F13&x=0&y=0 [1/31/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=1%2F31%2F13&x=0&y=0 [1/31/18]

18 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=1%2F31%2F08&x=0&y=0 [1/31/18]