WEEKLY QUOTE

“Silence is more musical than any song.”

– Christina Rossetti

WEEKLY TIP

About to start a business? Then be sure to file the correct forms with state government. Get in touch with your Secretary of State’s office (and your city and county) to see what licenses and forms you may need.

WEEKLY RIDDLE

Weight within my stomach, trees on my back, nails in my ribs, and feet I lack. What am I?

Last week’s riddle

There are 43 hikers walking toward a desert peak. On the way, 6 decide to hike another peak, 12 head back, and 25 make it to the peak. What happens to the rest of them?

Last week’s answer:

There are no more, 6 + 12 + 25 = 43.

HAS CONSUMER SPENDING MAINTAINED ITS PACE?

A new Department of Commerce report states that consumer spending rose 0.2% in February as consumer incomes improved 0.4%. These numbers replicated January’s gains. Even so, the personal savings rate hit a 6-month peak of 3.4% in February, suggesting that spending may have leveled off in the first quarter. Newly revised data shows that the economy was very healthy in the fourth quarter. Real consumer spending (personal spending adjusted for inflation) increased 4.0% while Gross domestic product expanded at a 2.9% annual rate. (The previous Q4 GDP estimate was 2.5%.)(1,2)

STILL PLENTY OF OPTIMISM ON MAIN STREET

Last week, the Conference Board announced a reading of 127.7 for the latest edition of its monthly consumer confidence index, not far from the outstanding mark of 130.0 it reached in February. The University of Michigan’s consumer sentiment index also fell slightly, declining to a final, impressive March mark of 101.4 from its preliminary reading of 102.0.(2)

PENDING HOME SALES INDEX POSTS A GAIN

The National Association of Realtors said that its gauge of housing contract activity rose 3.1% for February, even with seeming obstacles like a thin inventory of existing homes on the market and a scarcity of affordable properties. Pending sales were still down 4.1% year-over-year.(3)

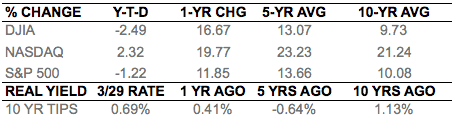

CHOPPY WEEK ENDS EVENTFUL QUARTER

After sizable advances and retreats across four trading sessions, the three major U.S. equity benchmarks ended higher for the abbreviated market week. The S&P 500 settled Friday at 2,640.87; the Nasdaq Composite, at 7,063.44; the Dow Jones Industrial Average, at 24,103.11. The S&P rose 2.03% in four trading days; the Nasdaq, 1.01%; the Dow, 2.42%.(4)

THIS WEEK: The Institute for Supply Management releases its March factory PMI Monday. Nothing major is scheduled for Tuesday. ISM’s March service sector PMI arrives Wednesday, plus a new ADP payrolls snapshot and earnings from CarMax and Lennar. New initial claims figures and the March Challenger job-cut report appear Thursday. On Friday, the Department of Labor presents its March employment report, and Federal Reserve chair Jerome Powell delivers a speech on the U.S. economic outlook in Chicago.

Sources: barrons.com, bigcharts.com, treasury.gov – 3/29/18(4,5,6,7)

Indices are unmanaged, do not incur fees or expenses, and cannot be invested into directly. These returns do not include dividends. 10-year TIPS real yield = projected return at maturity given expected inflation.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. The information herein has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. Investments will fluctuate and when redeemed may be worth more or less than when originally invested. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All market indices discussed are unmanaged and are not illustrative of any particular investment. Indices do not incur management fees, costs and expenses, and cannot be invested into directly. All economic and performance data is historical and not indicative of future results. The Dow Jones Industrial Average is a price-weighted index of 30 actively traded blue-chip stocks. The NASDAQ Composite Index is a market-weighted index of all over-the-counter common stocks traded on the National Association of Securities Dealers Automated Quotation System. The Standard & Poor’s 500 (S&P 500) is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy. NYSE Group, Inc. (NYSE:NYX) operates two securities exchanges: the New York Stock Exchange (the “NYSE”) and NYSE Arca (formerly known as the Archipelago Exchange, or ArcaEx®, and the Pacific Exchange). NYSE Group is a leading provider of securities listing, trading and market data products and services. The New York Mercantile Exchange, Inc. (NYMEX) is the world’s largest physical commodity futures exchange and the preeminent trading forum for energy and precious metals, with trading conducted through two divisions – the NYMEX Division, home to the energy, platinum, and palladium markets, and the COMEX Division, on which all other metals trade. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. MarketingPro, Inc. is not affiliated with any person or firm that may be providing this information to you. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional.

Citations.

1 – cnbc.com/2018/03/29/us-personal-income-feb-2018.html [3/29/18]

2 – investing.com/economic-calendar/ [3/29/18]

3 – nationalmortgageprofessional.com/news/66542/pending-home-sales-february [3/28/18]

4 – barrons.com/public/page/weekstocks.html [3/29/18]

5 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=3%2F29%2F17&x=0&y=0 [3/29/18]

5 – bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=3%2F29%2F17&x=0&y=0 [3/29/18]

5 – bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=3%2F29%2F17&x=0&y=0 [3/29/18]

5 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=3%2F28%2F13&x=0&y=0 [3/29/18]

5 – bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=3%2F28%2F13&x=0&y=0 [3/29/18]

5 – bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=3%2F28%2F13&x=0&y=0 [3/29/18]

5 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=3%2F28%2F08&x=0&y=0 [3/29/18]

5 – bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=3%2F28%2F08&x=0&y=0 [3/29/18]

5 – bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=3%2F28%2F08&x=0&y=0 [3/29/18]

6 – treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyield [3/29/18]

7 – treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyieldAll [3/29/18]

HAS CONSUMER SPENDING MAINTAINED ITS PACE?

A new Department of Commerce report states that consumer spending rose 0.2% in February as consumer incomes improved 0.4%. These numbers replicated January’s gains. Even so, the personal savings rate hit a 6-month peak of 3.4% in February, suggesting that spending may have leveled off in the first quarter. Newly revised data shows that the economy was very healthy in the fourth quarter. Real consumer spending (personal spending adjusted for inflation) increased 4.0% while Gross domestic product expanded at a 2.9% annual rate. (The previous Q4 GDP estimate was 2.5%.)(1,2)

STILL PLENTY OF OPTIMISM ON MAIN STREET

Last week, the Conference Board announced a reading of 127.7 for the latest edition of its monthly consumer confidence index, not far from the outstanding mark of 130.0 it reached in February. The University of Michigan’s consumer sentiment index also fell slightly, declining to a final, impressive March mark of 101.4 from its preliminary reading of 102.0.(2)

PENDING HOME SALES INDEX POSTS A GAIN

The National Association of Realtors said that its gauge of housing contract activity rose 3.1% for February, even with seeming obstacles like a thin inventory of existing homes on the market and a scarcity of affordable properties. Pending sales were still down 4.1% year-over-year.(3)

CHOPPY WEEK ENDS EVENTFUL QUARTER

After sizable advances and retreats across four trading sessions, the three major U.S. equity benchmarks ended higher for the abbreviated market week. The S&P 500 settled Friday at 2,640.87; the Nasdaq Composite, at 7,063.44; the Dow Jones Industrial Average, at 24,103.11. The S&P rose 2.03% in four trading days; the Nasdaq, 1.01%; the Dow, 2.42%.(4)

THIS WEEK: The Institute for Supply Management releases its March factory PMI Monday. Nothing major is scheduled for Tuesday. ISM’s March service sector PMI arrives Wednesday, plus a new ADP payrolls snapshot and earnings from CarMax and Lennar. New initial claims figures and the March Challenger job-cut report appear Thursday. On Friday, the Department of Labor presents its March employment report, and Federal Reserve chair Jerome Powell delivers a speech on the U.S. economic outlook in Chicago.

Sources: barrons.com, bigcharts.com, treasury.gov – 3/29/18(4,5,6,7)

Indices are unmanaged, do not incur fees or expenses, and cannot be invested into directly. These returns do not include dividends. 10-year TIPS real yield = projected return at maturity given expected inflation.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. The information herein has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. Investments will fluctuate and when redeemed may be worth more or less than when originally invested. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All market indices discussed are unmanaged and are not illustrative of any particular investment. Indices do not incur management fees, costs and expenses, and cannot be invested into directly. All economic and performance data is historical and not indicative of future results. The Dow Jones Industrial Average is a price-weighted index of 30 actively traded blue-chip stocks. The NASDAQ Composite Index is a market-weighted index of all over-the-counter common stocks traded on the National Association of Securities Dealers Automated Quotation System. The Standard & Poor’s 500 (S&P 500) is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy. NYSE Group, Inc. (NYSE:NYX) operates two securities exchanges: the New York Stock Exchange (the “NYSE”) and NYSE Arca (formerly known as the Archipelago Exchange, or ArcaEx®, and the Pacific Exchange). NYSE Group is a leading provider of securities listing, trading and market data products and services. The New York Mercantile Exchange, Inc. (NYMEX) is the world’s largest physical commodity futures exchange and the preeminent trading forum for energy and precious metals, with trading conducted through two divisions – the NYMEX Division, home to the energy, platinum, and palladium markets, and the COMEX Division, on which all other metals trade. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. MarketingPro, Inc. is not affiliated with any person or firm that may be providing this information to you. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional.

Citations.

1 – cnbc.com/2018/03/29/us-personal-income-feb-2018.html [3/29/18]

2 – investing.com/economic-calendar/ [3/29/18]

3 – nationalmortgageprofessional.com/news/66542/pending-home-sales-february [3/28/18]

4 – barrons.com/public/page/weekstocks.html [3/29/18]

5 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=3%2F29%2F17&x=0&y=0 [3/29/18]

5 – bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=3%2F29%2F17&x=0&y=0 [3/29/18]

5 – bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=3%2F29%2F17&x=0&y=0 [3/29/18]

5 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=3%2F28%2F13&x=0&y=0 [3/29/18]

5 – bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=3%2F28%2F13&x=0&y=0 [3/29/18]

5 – bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=3%2F28%2F13&x=0&y=0 [3/29/18]

5 – bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=3%2F28%2F08&x=0&y=0 [3/29/18]

5 – bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=3%2F28%2F08&x=0&y=0 [3/29/18]

5 – bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=3%2F28%2F08&x=0&y=0 [3/29/18]

6 – treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyield [3/29/18]

7 – treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyieldAll [3/29/18]